THE ADMINISTRATION’S PROPOSAL TO MAKE

THE TAX CUT PERMANENT

by Joel Friedman, Robert Greenstein, and Richard Kogan

| PDF of this report The Center issued a 2-page fact sheet on this subject on April 15, 2002. |

| If you cannot access the files through the links, right-click on the underlined text, click "Save Link As," download to your directory, and open the document in Adobe Acrobat Reader. |

Overview

President Bush has called for making permanent the tax cuts enacted last year, which are scheduled to expire by the end of 2010. The House Leadership intends to bring this proposal to a vote the week of April 15. Debate on locking these tax cuts into place for 2011 and all subsequent years comes at a time when new Congressional Budget Office projections show a dramatic deterioration in the budget outlook. The debate also comes only a few months after the President's Social Security Commission issued a report showing it was unable to come up with options to restore long-term Social Security solvency without drawing on large amounts of resources from the rest of the budget.

The proposal to make the tax cuts permanent by eliminating the 2010 "sunsets" in last year's tax-cut law carries a large price tag.

- In the first decade after 2012, the tax cuts would cost the Treasury approximately $4 trillion. This rather massive cost would come just as the baby boom generation begins to retire and the Social Security and Medicare systems come under increasing financial pressure. (This $4 trillion figure includes a Joint Committee on Taxation estimate of the cost of modest relief from the individual Alternative Minimum Tax; see the box on page 5. The $4 trillion figure assumes that CBO's 2012 estimate of the cost of last year's tax cut, if made permanent, remains a constant share of the economy after 2012. This is the standard approach CBO, GAO, and others take in projecting the long-term cost of tax cuts. It is conservative in this case because the costs of some provisions in this legislation, such as provisions affecting pensions and estates, are likely to grow faster than the economy. This figure does not include the large costs the tax cut would generate in additional interest payments on the debt.)

- An examination of the most recent report of the Social Security Trustees and of CBO's estimates of what the tax cut will cost when it is fully phased in indicates that if the tax cut is made permanent, its cost over the next 75 years will be more than twice as great as the entire 75-year shortfall projected in the Social Security Trust Fund.

These high costs are particularly striking in light of the marked deterioration in the fiscal outlook. The surpluses of a year ago have largely disappeared. The Congressional Budget Office now projects a surplus of $1.7 trillion over the 2002-2011 period, almost $4 trillion less than it projected a year ago. Moreover, even these more pessimistic projections substantially overstate the amount of the surplus that remains, according to experts such as former CBO director Robert Reischauer and the Senate and House Budget Committee staffs. They point out that the new CBO projections do not include the costs of a number of items — from increased defense and homeland security expenditures, to the farm bill, to the extension of a battery of popular expiring tax credits that always are extended, to name a few — that are virtually certain to be enacted in some form. These items are likely to remove at least another $1 trillion from the projected surplus for the next ten years, and what little projected surplus then remains may never materialize, given the uncertainty of ten-year forecasts.

Extending the tax cuts permanently, as the Administration is proposing, would only worsen the already deteriorating fiscal outlook over the next decade. Doing so would enlarge the deficits outside Social Security and increase the extent to which funds would have to be borrowed from the Social Security Trust Fund to cover other governmental costs. This concern pales, however, beside the problems that making the tax cut permanent would pose in years after 2012. While long-range forecasts are inherently uncertain, there are some things we know for sure about the decades that lie ahead. Specifically, we know the baby-boom generation will begin to retire in large numbers during the second decade of this century and that the cost of Social Security, Medicare, and Medicaid long-term care will rise substantially as a result. Yet if the tax cut is made permanent, it is during that same decade that its cost will explode, as all of its revenue-losing provisions will then be fully in effect.

Making the tax cut permanent will not only strain the budget but will also do little to improve economic growth. Recent analyses by Brookings Institution economists William Gale and Peter Orszag persuasively refute assertions made by supporters of the tax cut that it will have a strong positive impact on the economy. In the Gale study, which stands as the most rigorous and comprehensive examination to date of the likely effects of the tax cut, Gale and his co-author Samara Potter conclude that the tax cut is more likely to reduce the size of the economy over time than to increase it. Orszag finds that making the tax cut permanent would not stimulate the economy now, since research shows people tend not to spend tax cuts until they actually receive them, and would do little for the economy over the long term. Both analyses point out that any long-term economic benefits from the bill's reduction of marginal tax rates are offset by the measure's high cost, which reduces national saving and exerts upward pressure on long-term interest rates.

The Administration's proposal to make the tax cut permanent — and to add new tax cuts on top of it — stands in sharp contrast to the response of an earlier tax-cutting President when the fiscal situation clouded. President Ronald Reagan secured a large tax cut in 1981, as President Bush did in 2001. And 20 years ago, as today, the fiscal situation deteriorated significantly in the year after the tax cut was enacted. Then, however, the Reagan Administration responded by working with Congress, behind the leadership of Senate Finance Committee chairman Bob Dole, to enact revenue measures to undo or offset a significant share of the revenue loss from the recently enacted tax cut, as part of an effort to improve the nation's long-term fiscal position. The Bush Administration's proposals to make the tax cut permanent and add new tax cuts on top of it chart precisely the opposite course.

The Cost of Making the Tax Cuts Permanent

Almost half of the tax cuts enacted last June are already in effect. The remainder phase in throughout the decade. Some of the tax cuts already in effect are scheduled to expire in 2004, 2005, or 2006. All provisions of the tax cut are scheduled to expire by the end of 2010. (See the Appendix for a schedule of when various provisions of the tax cut phase in and expire.)

| without interest | with interest | ||

| Costs from 2001 through 2012: | |||

| tax cut as enacted last June | $1,290 billion | $1,756 billion | |

| cost of eliminating the 2010 "sunsets" | + 374 | + 397 | |

| cost of providing modest AMT relief* | + 363 | + 423 | |

| tax cut if extended, including AMT relief* | 2,027 | 2,577 | |

| Second decade (2013-2022) | $4.1 trillion | $7.1 trillion | |

| 75-year costs (present value as a share of GDP): | |||

| tax cut if extended, including AMT relief* | 1.68% of GDP | ||

| net shortfall in the Social Security trust fund | 0.72% of GDP | ||

| * increases the AMT exemption amount so that the number of tax filers subject to the AMT grows to "only" 20.5 million in 2011, as under prior tax law. Also includes the extension of two small provisions of the tax cut scheduled to expire after 2005 or 2006. Amounts may not add due to rounding. | |||

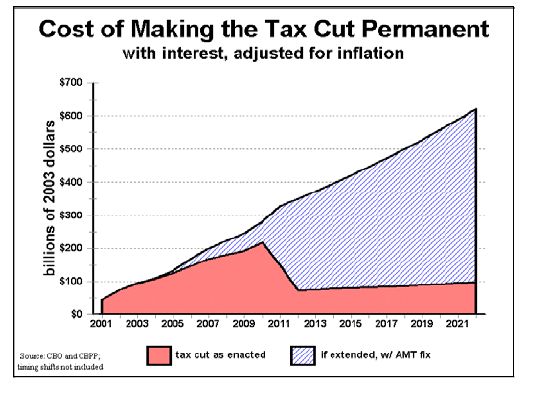

Costs Through 2012

According to CBO, making permanent the provisions in the last year's tax-cut package that are scheduled to expire at the end of 2010 would cost $374 billion through 2012, or $397 billion when the increased interest payments on the debt are included. These added costs would aggravate the already large deterioration in the budget surplus. If the tax cut is made permanent, CBO figures show that the budget outside Social Security would run an overall deficit of $500 billion between 2003 and 2012.

The Cost of the Tax Cut Compared to the Costs of Various Federal Agencies One way to grasp the magnitude of the tax cut when it becomes fully effective — and of the costs of making the tax cut permanent — is to compare the tax cut's cost when it is fully in effect to the costs of various federal agencies. When fully effective, the tax cut will be —

The tax cut is skewed to those with the highest incomes. (The degree to which the tax cut favors the well off may not be readily apparent today because the aspects of it that are already in effect tend to be the most progressive while the aspects not yet in effect are highly regressive overall.) When the entire tax cut is fully in effect, the tax cuts conferred on the wealthiest one percent of taxpayers will be equal in cost to —

Comparable figures for the tax cut and agency budgets are calculated as follows: agency budget are the average of the annual expenditures OMB shows for 2001, 2002, and 2003; the size of the tax cut is an estimate of its costs in 2002 if all of its provisions had been fully effective by the beginning of 2001. The share of the fully-effective tax cut applicable to the wealthiest one percent of the population was calculated by William G. Gale of the Brookings Institution. |

Moreover, these estimates present a view of the tax cut and the budget outlook that is likely to be too optimistic. The estimates just cited reflect CBO projections that follow prescribed rules for establishing the budget "baseline" and therefore exclude a variety of costs that are almost certain to be incurred. As Robert Reischauer, president of the Urban Institute and former director of CBO, observed in recent testimony before the Senate Budget Committee, "it will be very difficult to adhere to the fiscal restraint in the baseline and so the baseline projections may prove to be a somewhat misleading indicator of the attainable, let alone the likely, future budget outlook. Rarely have the policies underlying the baseline projections been as disconnected from the policy makers' agendas as they are today."(1) The chairmen and ranking members of the House and Senate Budget Committees came to a similar conclusion last October when they assessed the fiscal outlook.

The Issue of the Alternative Minimum Tax Another example of a virtually inevitable cost that is not reflected in the CBO baseline is the cost of preventing the individual Alternative Minimum Tax from exploding in size and encroaching heavily upon middle-class taxpayers in years ahead. The cost of such relief also is left out of the CBO estimates of the cost of repealing the 2010 sunsets on the tax cut and making the tax cut permanent. Such relief is certain to be provided, however, to prevent the number of taxpayers subject to the AMT from growing by nearly 2000 percent over the coming decade, as would occur under current law. Fewer than two million taxpayers are currently subject to the AMT. The Treasury Department estimates that, in no small part because of last year's tax-cut law, the number of taxpayers subject to the AMT will soar by 2012 to 39 million — about one of every three taxpayers in the nation — assuming the tax cuts are made permanent. Many middle-class families would find themselves subject to the AMT, and the swollen AMT would "take back" much of the tax cut from many of the tax filers it would affect. It is inconceivable the President or the Congressional leadership of either party will allow the AMT to mushroom in this manner. The tax-cut bill enacted last year includes an AMT relief provision to avert this outcome; the provision is designed to ensure that the tax-cut legislation does not cause millions of additional taxpayers to become subject to the AMT. However, because the cost of this provision would have driven the tax cut's cost well above what last year's Congressional budget resolution allowed, the framers of the tax cut resorted to a gimmick: they sunset this AMT relief provision at the end of 2004, knowing that Congress would have no choice but to extend AMT relief before the provision expired. The Administration's current proposal to make the tax cut permanent employs the same gimmick. While lifting the 2010 sunsets in last year's tax-cut legislation, the proposal leaves the 2004 sunset of the AMT relief provision in place. This conveniently reduces the apparent cost of making the tax cut permanent. The cost estimates that CBO and the Joint Committee on Taxation have provided for the Administration's proposal to make the tax cut permanent are based on the assumption that the AMT relief provision will terminate after 2004 and thus that one of every three taxpayers in the nation will be subject to the AMT by 2012, with these taxpayers having the size of their tax cuts reduced by this swollen AMT. Use of this gimmick virtually guarantees that Congress will have to pass yet another large tax cut bill by 2004 to avert an impending AMT explosion. In short, the cost of extending AMT relief beyond 2004 is essentially an "off-book liability" that must be considered a part of the long-term cost of the Administration's proposal to make the tax cut permanent (particularly given that the Administration has provided no indication it would countenance scaling back parts of the enacted tax-cut package or raising other taxes to pay for the cost of this inevitable AMT relief). In projecting the costs of making the tax cut permanent over the second decade and over 75 years, this analysis therefore includes the cost of extending the AMT relief provision beyond 2004. That provision was designed to limit the increase through 2004 in the number of tax filers affected by the AMT to the level it would have attained under the tax law in effect prior to enactment of last year's legislation. This analysis reflects the cost of extending the expiring AMT relief provision beyond 2004 to achieve the same result (i.e., so it continues to limit the increase in the number of tax filers subject to the AMT in years after 2004 to the levels that would have been reached under prior law). This approach produces a conservative cost estimate, since it assumes that policymakers will allow the number of filers subject to the AMT to increase to more than 20 million by 2011, as would have been the case under the prior law. |

For example, the CBO estimates do not take into account the significant increases in defense and homeland security expenditures that the President has proposed, most or all of which are sure to be enacted. Nor do they include the cost of other program extensions and tax reductions that are virtually certain to be enacted, such as the pending farm bill and the extension of various tax credits and other tax provisions that are scheduled to expire every few years but always are routinely extended. It is also a near certainty that Congress will feel compelled to provide relief from the individual Alternative Minimum Tax to prevent the number of taxpayers subject to the AMT from swelling from about two million today to 35 million by 2010 under current law, growing to 39 million by 2012 if the tax cut is made permanent (see box on page 5). Overall, the CBO projections do not include $1 trillion or more in likely costs over the coming decade.

In fact, if the tax cut is made permanent and modest AMT relief is enacted, but no other new costs are recognized, the budget outside of Social Security will be in deficit in every year through 2012. Given current forecasts, it appears that permanent tax cuts mean permanent deficits. Even if Social Security surpluses are counted, the combination of these unrecognized costs — defense increases, homeland security, a farm bill, AMT relief — and the extension of the tax cut would essentially deplete what remains of the surplus in the unified budget through 2012. As a result, there would be little or no debt reduction for the remainder of the decade. This stands in sharp contrast to a year ago when the Administration presented a budget that boasted ten-year unified-budget surpluses totaling $5.6 trillion and claimed that an expensive tax cut plus a range of other costly initiatives were eminently affordable and would leave enough of the surplus to eliminate most or all of the national debt.

Costs After 2012

Despite significant concerns about the coming decade, the principal fiscal impacts of making the tax cut permanent would occur in years after 2012. The cost of the tax cut over the first ten years is artificially low, held down by the slow phase-in of various provisions of that legislation. If the tax cut were permanently extended, all of its provisions would be fully in effect by 2011, and the budget would have to bear the full cost of these measures in the years after that.

- For the ten years from 2013 to 2022, the cost of the tax cut would be approximately $4 trillion, based on estimates that CBO has issued of the legislation's cost in 2011. (When the costs of the increased interest payments on the debt are included, the total cost rises to more than $7 trillion.

- Over the next 75 years, the cost of the tax cut — if made permanent — would be more than twice as great as the shortfall in the Social Security Trust Fund. The Social Security actuaries and Trustees project that the Social Security shortfall is equal to 0.72 percent of the gross domestic product over the next 75 years.(2) The tax cut would cost 1.68 percent of GDP over that period.(3)

This comparison with Social Security is particularly significant, not only because it places the large size of the tax cut in perspective but also because the cost of the tax cut would, if made permanent, reach its full dimensions in the same period that the baby-boom generation begins to retire in large numbers and Social Security and Medicare costs swell as a result. Approval of the proposal to make the tax cut permanent would result in a permanent revenue loss that would occur largely outside the 10-year "budget window" that Congress uses, but would coincide with the baby boomers' retirement. As CBO Director Dan Crippen observed in testimony before the Senate Budget Committee on January 23, "long-term pressures on spending loom just over the horizon. Those pressures result from the aging of the U.S. population (large numbers of baby boomers will start becoming eligible for Social Security retirement benefits in 2008 and for Medicare in 2011), from increased life spans, and from rising costs for federal health care programs."(4)

Furthermore, substantial revenues from outside Social Security are likely to be needed to ensure the solvency of the Trust Fund if drastic Social Security benefit cuts are to be avoided, a point illuminated by the recent report of the President's Commission to Strengthen Social Security. The President's hand-picked Commission presented three options, one of which failed to restore solvency to the Trust Fund. The other two options were able to eliminate the shortfall in the Trust Fund and restore long-term solvency only by relying both on substantial cuts in traditional Social Security benefits (cuts likely to be too large to be acceptable politically) and the transfer of trillions of dollars in revenue from the rest of the budget to Social Security or private accounts. Permanent extension of the tax cut would render it virtually impossible to make such transfers to Social Security unless rather severe cuts were made elsewhere in the budget or sizeable tax increases were enacted. Permanent extension of the full tax cut thus would risk eliminating the resources that ultimately will be needed if long-term Social Security solvency is to be restored without deep Social Security benefit cuts or sizeable payroll tax increases. Permanent extension of the full tax cut also would make it less likely that Congress will ever be able to find the resources to provide a significant prescription drug benefit for seniors (except for those with the lowest incomes).

Economic Impact of Making Tax Cuts Permanent

Supporters of the proposal to make the tax cut permanent often tout the positive impact this will have on the economy. But recent analyses by Brookings Institution economists have found that the tax cuts enacted last year are more likely to have a negative rather than positive impact on the economy. For example, William Gale and Samara Potter found that the tax-cut package "reduces the size of the future economy, raises interest rates, makes taxes more regressive, increases tax complexity, and was fiscally unsustainable even before the economic downturn and the terrorist attacks slowed the economy in 2001."(5) Given the conclusions of this analysis, which is the most comprehensive and rigorous study to date of the tax cuts' likely fiscal and economic impacts, there is little economic rationale for making these tax cuts permanent.

Another Brookings Institution economist, Peter Orszag, explained convincingly in testimony before the Senate Budget Committee in January that making the tax cut permanent will not, as some assert, generate increased economic activity today.(6) Orszag noted that the argument that future tax cuts can have significant effects on economic activity today, which assumes that consumers and businesses will take into account future tax savings and will increase their spending immediately, is belied by studies of previous tax cuts that phased in over time. He reported: "These studies strongly suggest that people tend not to spend tax cuts prospectively; instead, they largely wait until the money is in their pockets."

Orszag's well-documented testimony also rebuts the contention that making the tax cut permanent would have a positive long-term impact on the economy. Reaching much the same conclusion as Gale and Potter, Orszag explains that the enacted tax cuts are likely to boost long-term economic growth only slightly, and that these small positive effects are likely to be offset by the negative effects the tax cut would have in reducing national saving by depleting projected budget surpluses or increasing projected budget deficits. Orszag observed that "any positive incentive effects from lower tax rates in the long run are offset by the adverse effects from lower national savings. The overall effect of the yet-to-be-implemented tax cuts on economic activity in the long run may, if anything, be negative."

Distribution of the Tax Cut Benefits

When all of the enacted tax cuts are fully in effect, the benefits will flow disproportionately to those with the highest incomes. The 1.3 million tax filers who make up the most affluent one percent of filers will receive more than one-third of the tax cuts. (The previously discussed analysis of the tax cut by Brookings Institution economists William Gale and Samara Potter estimates that when the tax cut is fully in effect, the top one percent of tax filers will receive 36.7 percent of the tax cuts.) The 1.3 million tax filers in this elite group will receive about twice as much in tax cuts as the 78 million low- and moderate-income filers who comprise the bottom 60 percent of filers.(7) Permanent extension of the entire tax cut would perpetuate this skewed distribution.

It should be noted that the distribution of the tax cuts that are in effect today is very different from what the distribution of the tax cuts will be when the tax cut is phased in fully. About 70 percent of the tax cuts that will benefit middle-income families — and an even higher percentage for families who are less well off — have already taken effect. In contrast, a substantial majority of the tax cuts that are slated to go the top one percent of tax filers have yet to go into effect. The reductions in tax rates in the top income tax brackets, the repeal of limitations in current tax law on the use of personal exemptions and itemized deductions by high-income individuals, and the repeal of the estate tax — all measures that would primarily or exclusively benefit the most well-off — phase in slowly over a number of years.

In his State of the Union address, the President declared that "most Americans thought tax relief was just right" when they received their rebate checks last summer. But while this may be true, it is a bit misleading. Many Americans' response to the tax cut is likely to be shaped by the level of tax relief in effect now, not the level that will be in effect at the end of the decade and that the President is proposing to lock in on a permanent basis. For the bulk of taxpayers, the current level of tax relief will not increase much over the decade, but for those with the highest incomes, the magnitude of the tax cuts will swell dramatically.

Uncertainty of Long-Range Projections

As the stunning shift in the budget outlook over the past year demonstrates, there is considerable uncertainty inherent in multi-year projections. Organizations such as the Concord Coalition and the Center on Budget and Policy Priorities raised this point during the tax-cut debate last year, calling for smaller tax cuts (except for temporary tax cuts while the economy was weak) until it was clear that projected surpluses would materialize. Furthermore, when issuing its revised budget projections this January the Congressional Budget Office warned: "Budget projections are always subject to considerable uncertainty. However, that uncertainty is particularly great this year as the nation continues to wage war on terrorism and recover from a recession."(8)

An Alternative Proposal Urban Institute president Robert Reischauer and Brookings Institution senior fellows Peter Orszag and William Gale have proposed alternatives to a permanent extension of all of the enacted tax cut.* These alternatives would address some of the problems associated with the Administration's approach. While varying slightly in the details, their proposals call for making permanent those tax cuts already in place, while postponing the remaining tax cuts until they are found to be affordable.

_______________ *See the testimony of Peter Orszag and Robert Reischauer before the Senate Budget Committee, January 29, 2002. |

When promoting its tax cut last year, the Administration exhibited strong confidence in long-term forecasts. That now has changed. More recent comments by Administration officials, including Treasury Secretary Paul O'Neill and OMB director Mitchell Daniels, imply they no longer find ten-year budget estimates trustworthy.(9) The House Budget Committee majority echoed these concerns about the reliability of ten-year estimates when it departed from recent practice and limited this year's budget resolution to a five-year period.

There is, however, an inconsistency here. How can the Administration and the House leadership propose permanent extension of the tax cut if the fiscal outlook is so uncertain beyond the five-year point? If they have so little confidence in long-term budget estimates, how do they reach the conclusion that the full tax cut is affordable on an ongoing basis?

Adding to questions about the tax-cut's long-term affordability is the basic reality that while long-range economic forecasts carry a high degree of uncertainty, no such uncertainty surrounds the fact that the baby boom generation will soon begin reaching retirement age. When these individuals retire, the country will have to finance their retirement benefits and medical care at a cost that ultimately will be beyond the means of the current Social Security and Medicare trust funds. Regardless of how accurate the current long-term economic projections turn out to be, there is little doubt that the nation faces long-term financing problems in Social Security and Medicare. As a result, when the sobering demographic realities are viewed in conjunction with the uncertainties about the long-term performance of the economy, the conclusion seems inescapable that policymakers should adopt a more cautious and prudent approach than making the full tax cut permanent at a cost of $4 trillion in the second decade of this century.

APPENDIX 2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

|

End Notes:

1. Robert D. Reischauer, "Framing the Budget Debate for the Future," Testimony before the Senate Budget Committee, January 29, 2002.

2. The 2002 Annual Report of the Board of Trustees of the Federal Old-Age and Survivors Insurance and Disability Trust Funds, March 26, 2002, page 164.

3. Richard Kogan, Robert Greenstein, and Peter Orszag, "Social Security and the Tax Cut," Center on Budget and Policy Priorities, revised April 11, 2002.

4. Dan L. Crippen, "The Budget and Economic Outlook: Fiscal Years 2003-2012," Testimony before the Senate Budget Committee, January 23, 2002.

5. William G. Gale and Samara R. Potter, "An Economic Evaluation of the Economic Growth and Tax Relief Reconciliation Act of 2001," National Tax Journal, forthcoming. Available on the Brookings Institution website at http://www.brookings.org/views/articles/gale/200203.htm

6. See Peter R. Orszag, "The Budget and the Economy," Testimony before the Senate Budget Committee, January 29, 2002; and Peter Orszag and Robert Greenstein, "Future Tax Cuts and the Economy in the Short Run", Center on Budget and Policy Priorities, January 28, 2002.

7. Isaac Shapiro, Robert Greenstein, and James Sly, "Under Conference Agreement, Dollar Gains for Top One Percent Essentially the Same as Under House and Bush Packages," Center on Budget and Policy Priorities, May 26, 2001.

8. Congressional Budget Office, "The Budget and Economic Outlook: Fiscal Years 2003-2012," January 2002.

9. Treasury Secretary Paul O'Neill stated on January 6,2002, on Meet the Press: "I think that people who believe as a religion in 10-year numbers haven't lived in the real economy...And so to make a big deal out of 10 years seems to be a false idea."