SMALL BUSINESSES BENEFIT MUCH LESS THAN ADVERTISED FROM ADMINISTRATION TAX CUTS

|

PDF of this analysis

Related

Report |

|

| If you cannot access the files through the links, right-click on the underlined text, click "Save Link As," download to your directory, and open the document in Adobe Acrobat Reader. |

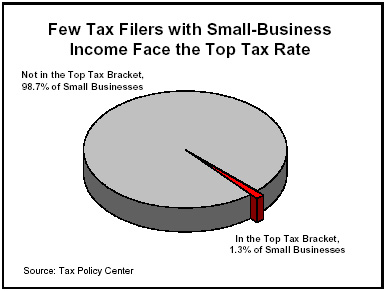

A new Center report, Administration Tax-Cut Rhetoric and Small Businesses, shows the Administration has seriously exaggerated the benefits of its tax cuts to small businesses, especially the reduction in the top marginal tax rate and the repeal of the estate tax. The vast majority of small businesses receive no benefit whatsoever from those two tax cuts. Moreover, the majority of the benefits that small businesses receive from the tax cuts enacted since 2001 go to an elite group of owners with considerable wealth and high incomes.

- Only about 1 percent of small businesses benefit from the reduction

in the top rate. Only 436,000 tax filers with small-business

income — just 1.3 percent of the 32.8 million filers in the nation with

small-business income — are subject to the top tax rate, according to the

Urban Institute-Brookings Institution Tax Policy Center.

The filers with small-business income who do face the top rate hardly fit the popular image of “small-business owners”: their average income in 2004 is $1.5 million. (The Tax Policy Center used the Treasury Department’s broad definition of “small-business owner,” which includes businesses that are not small and wealthy investors who have nothing to do with operating the business. President Bush and Vice President Cheney would both qualify as “small-business owners” under the Treasury definition.)

-

Only a miniscule number of small businesses are affected by

the estate tax. The Administration argues that making estate-tax repeal

permanent is essential for small businesses and farms, because estates with

small businesses or farms otherwise will face the prospect of having to

liquidate the enterprise to pay the estate tax.

Only a miniscule number of small businesses are affected by

the estate tax. The Administration argues that making estate-tax repeal

permanent is essential for small businesses and farms, because estates with

small businesses or farms otherwise will face the prospect of having to

liquidate the enterprise to pay the estate tax.

The Tax Policy Center has examined the impact of the estate tax on small businesses and family farms. Its analysis defines a “small” business or farm as one worth $5 million or less and focuses on estates in which the business or farm constitutes a majority of the assets in the estate. (If the business or farm represents only a minority of the assets, the other assets can be used to pay the estate tax and thereby shield the business or farm from liquidation.)

The Tax Policy Center found that in 2004, only 340 estates nationwide that contain a business or farm worth up to $5 million and in which the business or farm constitutes the majority of the estate will face any estate tax. The Tax Policy Center also estimates that in 2009, only 50 such estates — or just one per state, on average — will be subject to the estate tax; all other estates in which a small business or farm constitutes the majority of the estate will be exempt. (In 2004, estates valued at less than $1.5 million for an individual and $3 million for a couple are exempt from the tax. By 2009, those levels will rise to $3.5 million and $7 million, respectively.)

Accordingly, despite the high cost of estate tax repeal, only a tiny number of small businesses and farms will be affected when the large estate-tax exemptions that will be in place in 2009 give way to full repeal of the estate tax in 2010.

- The tax cuts enacted since 2001 heavily favor “small-business owners” with very high incomes. Some 51 percent of the tax cuts going to households with small-business income are accruing to the 8 percent of such households that have incomes exceeding $200,000. By contrast, only 16 percent of the tax cuts for households with small-business income are going to the 62 percent of such households with incomes below $75,000.

-

The tax cuts will likely have only a minor impact on the

economy. The Administration emphasizes the benefits of its tax cuts for

small businesses in making the case that the tax cuts will spur major economic

and job growth. However, studies by the Joint Committee on Taxation and CBO

find that the tax cuts can be expected to have only minor economic effects

over the next ten years.

Further, studies by economists at the Brookings Institution and other institutions also conclude that if the tax cuts are made permanent, their long-term effects may be negative, as their high cost swells the already-unsustainable deficits the nation faces. The adverse long-term effects of these deficits, such as raising the cost of capital for new investment and reducing long-term investment and economic growth, would apply to small and large businesses alike.