ENTITLEMENT CAP WOULD REQUIRE DEEP CUTS IN ENTITLEMENT PROGRAMS

by Richard Kogan and Robert Greenstein

Summary

|

Summary:

HTM |

PDF Full Report: PDF |

| If you cannot access the files through the links, right-click on the underlined text, click "Save Link As," download to your directory, and open the document in Adobe Acrobat Reader. |

Budget legislation introduced in May by Rep. Jeb Hensarling and 58 House co-sponsors (H.R. 2290) includes a provision that would impose an annual cap on expenditures for entitlement programs other than Social Security.[1] The cap would be set at levels that would require entitlement programs to be cut by $2.1 trillion over the next ten years.

This legislation is now being considered in discussions that the House Leadership has instituted among House Republican leaders, various committee chairmen, and other Members. These discussions are intended to produce budget legislation that the Leadership has said it intends to move some time after the August recess.

Under the entitlement cap provision in H.R. 2290, a limit would be imposed each year on total expenditures for entitlement programs other than Social Security. These annual caps would be set at levels significantly below what the entitlement programs are projected to cost under current law, and cuts of sufficient magnitude would have to be made to fit entitlement costs within the caps. The caps are designed in such a manner that with each passing year, they fall farther below what the entitlement programs would cost under current law, necessitating steadily deepening cuts to meet the caps. In any year that Congress and the President failed to cut entitlements enough to fit within the cap for that year, automatic cuts in entitlement programs would be triggered.

The Depth of the Cuts

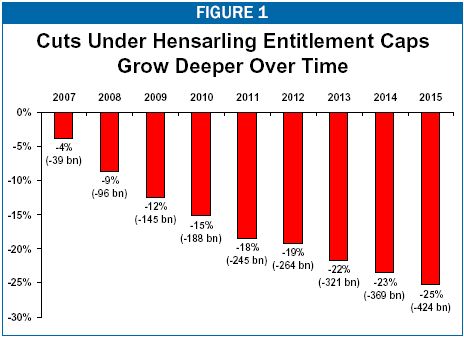

The Congressional Budget Office issues detailed cost projections and related data on entitlement programs, and analysts can use these data and projections to estimate the levels at which the entitlement caps would be set under the Hensarling proposal. The CBO projections and data show that over the ten years ending in 2015, the entitlement caps would be set a total of $2.1 trillion below the projected cost of entitlement programs under current law. The proposal thus would mandate $2.1 trillion in cuts over the coming decade.

|

Medicare |

$919 |

|

Medicaid |

460 |

|

Federal civilian

retirement and disability |

127 |

|

Military retirement

and disability |

74 |

|

Unemployment

compensation |

73 |

|

Earned Income and

Child Tax Credits |

72 |

|

Supplemental

Security Income |

69 |

|

Veterans’ benefits

|

56 |

|

Food Stamps |

54 |

|

TANF and other

family support |

37 |

|

Child Nutrition |

25 |

|

Commodity Credit

Corporation price supports |

21 |

|

TRICARE for life |

16 |

|

Other federal

retirement and disability |

15 |

|

Foster Care and

Adoption Assistance |

13 |

|

Student loans |

13 |

|

Universal Service

Fund |

11 |

|

State

Children’s

|

8 |

|

Social services

(Title XX, voc rehab) |

7 |

|

Other miscellaneous |

22 |

|

|

|

|

TOTAL |

2,092 |

In 2015 alone, the required cuts would reach $424 billion. This would require the elimination by 2015 of more than one of every four dollars that would otherwise be provided in entitlement benefits.

Why the Cuts Would be So Large

The required cuts would be this large for two reasons: the proposal’s failure to take increases in health care costs into account in setting the level of the entitlement caps, and the proposal’s inclusion of interest payments on the national debt as an entitlement program.

- Under the proposal, the entitlement cap for each year would be set at a level equal to the sum of the costs of all entitlement programs except Social Security in the prior fiscal year, with two adjustments. An adjustment would be made for projected increases or decreases in the number of people eligible for each entitlement program. The second adjustment would incorporate, for each program, the cost-of-living adjustment required in that program’s governing statute or the projected increase in the Consumer Price Index, whichever was greater.

- These two adjustment factors,

however, ignore the fact that Medicare and Medicaid costs rise with increases

in the cost of health care, not with increases in the Consumer Price

Index. As is well known, health care costs are rising rather rapidly in the

private and public sectors alike and are increasing at a considerably faster

pace than the general inflation rate. The Hensarling entitlement cap is set

at a level that makes room for Medicare and Medicaid costs per beneficiary to

rise at an average rate of only 2.4 percent per year over the coming

decade, far below the expected rate of increase in health care costs.

Hardly any employer in America can hold increases in health insurance premiums to 2.4 percent per beneficiary per year. Health care costs are climbing much faster than that. Accordingly, CBO projects that Medicare and Medicaid costs will grow at an annual average rate of 6.3 percent per beneficiary over the coming decade, far above the 2.4 percent that the Hensarling caps make room for. This difference between the projected increases in health care costs per beneficiary in Medicare and Medicaid and the much smaller adjustments the Hensarling proposal would allow would cause a $1 trillion divergence between projected entitlement costs and the entitlement caps. The proposal’s failure to take rising health care costs into account thus would require $1 trillion in entitlement cuts. Moreover, because any entitlement (except Social Security) could be cut to comply with the cap, all entitlements other than Social Security — not just Medicare and Medicaid — would be at risk of steep cuts.

- Exacerbating

these problems, the Hensarling proposal treats interest payments on the debt

as an entitlement program. Whenever interest payments rose faster than

inflation, the entitlement cap would be breached and additional cuts in

entitlement programs would be mandated. (Interest costs cannot themselves be

cut directly.) The inclusion of interest payments within the entitlement cap

is extremely significant since interest payments are projected to rise sharply

over the coming decade, both because interest rates are expected to

climb from their current unusually low levels and because the amount of debt

on which interest will be paid will continue to escalate, as the government

continues to rack up large deficits each year.

Of particular note, if the 2001 and 2003 tax cuts are extended without being “paid for,” deficits and debt — and hence interest payments on the debt — will be even greater than they otherwise would be. Under the proposed entitlement cap, action to extend the tax cuts consequently would trigger deeper cuts in entitlement programs. In fact, each time that Congress enacted a new tax cut without paying for it, interest costs would rise further and cause entitlement programs to have to be cut more severely. Assuming that the existing tax cuts and relief from the Alternative Minimum Tax are continued, the projected growth of interest costs over the coming decade would necessitate an additional $1.1 trillion in entitlement cuts under the proposal, beyond the $1 trillion necessitated by Medicare and Medicaid cost growth.

- The combined effect of these two factors — health care costs and interest payments — is that entitlement programs would have to be cut $2.1 trillion over the next ten years to fit within the entitlement caps.

- Even deeper cuts would be required if various events that are beyond policymakers’ control occurred and caused entitlement expenditures to increase. For example, a flu epidemic or the onset of some other major disease could cause Medicare and Medicaid costs to rise, while an improvement in international harvests could cause farm prices to fall — and farm price support costs to increase (see box on page 6). These and other such unforeseen developments that cause entitlement costs to rise cannot be predicted in advance and may not pose ongoing budgetary threats (because the spike in expenditures ends when the event that triggered the spike passes). Moreover, entitlement programs exist, in part, as insurance against such unforeseen events. The proposed entitlement cap, however, generally would require deeper cuts in entitlement programs when such events occur. The cap would thereby undercut the safety-net or insurance nature of these programs, forcing deeper cutbacks in these or other programs in the very years they are most needed.

How Would Particular Programs be Affected?

How deeply would Congress cut a particular program to meet the caps? The exact size of the cutbacks in each program would depend on decisions that Congress and the President would make. In theory, Congress and the President could initially decline to enact any legislation cutting entitlement programs and let automatic entitlement cuts do all of the “dirty work.” Under the proposal’s rules for automatic cuts, some programs (such as Medicare hospital insurance) would be exempt from the automatic cuts, and certain other programs (such as veterans’ programs, Medicare physicians’ coverage, the new drug benefit, and Medicaid) would be cut no more than two percent through an automatic cut. (It should be noted that all cuts would be permanent, and that programs in which the automatic cut would not exceed two percent would be reduced an additional two percent each time an automatic cut occurred. As a result, the automatic cuts in these programs could mount to substantial levels over time. If automatic cuts occurred every year, these programs could be cut as much as 17 percent — or one-sixth — by 2015.)

It is unthinkable, however, that the bulk of the reductions would occur through automatic cuts. The automatic cuts are designed to be so unpalatable that Congress and the President would feel compelled to enact legislation making cuts in various entitlements in order to avert (or minimize) the automatic cuts. If all of the reductions needed to comply with the proposed entitlement cap were made through automatic cuts, then programs that would be fully subject to the automatic cuts (i.e., the programs that would have no protection from the automatic cuts) would be entirely eliminated by 2010. Those programs include, among others, farm-price supports and crop insurance, extended unemployment benefits and trade adjustment assistance, the Earned Income Tax Credit, vocational rehabilitation, child care payments to states, and the Social Services Block Grant (Title XX) — as well as the salaries of Senators Member of Congress.

Needless to say, it is inconceivable that Congress would sit idly by and allow these programs — and Members’ own salaries — to be eliminated. Congress clearly would seek to spread the pain more broadly by enacting legislation that cut more heavily into entitlement programs that had some protection from the automatic cuts, such as Medicare and Medicaid. It is important to understand that when the Hensarling proposal exempts a particular entitlement program from automatic cuts, it does not exempt that program from cuts that Congress could enact to meet the caps. The only truly protected program would be Social Security, because only Social Security would be outside the caps.

The bottom line is that all entitlement programs except Social Security would be at serious risk of being cut deeply, given that $2.1 trillion in reductions would be mandated over the next ten years. The table on page 2 shows the magnitude of the cuts that would be made in each entitlement program over the next ten years if all programs other than Social Security were cut by the same percentage.

|

Broad-based Opposition to Entitlement Cap Proposal

Last year, a broad array of organizations expressed strong

opposition to entitlement-cap proposals.

For example, in a letter to Speaker Dennis Hastert on

|

Additional Issues Raised by the Proposal

Four additional points are worth noting. First, the required entitlement cuts would reach more than 25 percent — more than one dollar in every four — by 2015. In programs such as veterans’ disability benefits or food stamps, the benefits that each person receives could be cut by one quarter. The situation is different, however, in Medicare and Medicaid. Those programs deliver benefits by paying doctors and hospitals to provide health care to people who are elderly or disabled or have low income. If doctors and hospitals were paid 25 percent less, many or most would likely choose not to treat those patients, and the programs could collapse. The only plausible ways to cut Medicare and Medicaid by 25 percent are to reduce sharply the number of elderly, disabled, or low-income people who are eligible for public health insurance (for example, by raising to well above 65 the age that a person must attain to become eligible for Medicare), or to require sick people to make up for federal reductions in payments to health-care providers by paying more out of their own pockets. People who are poor — as well as many middle-income elderly and disabled people who have serious illnesses or medical conditions that require extensive treatment — would likely have great difficulty affording the large added out-of-pocket costs that would result.

Second, under the proposed cap, deep cuts would continue to occur even in years when the economy is weak, which could push a faltering economy into recession or cause an existing recession to become deeper and more protracted. Moreover, during economic downturns, Congress often enacts temporary increases in some benefits, such as extensions of unemployment insurance benefits and temporary increases in federal matching payments for Medicaid. Such legislation provides relief to families in distress while also helping to stabilize the economy. The proposed cap could make the enactment of such forms of economic stimulus more difficult (because the stimulus measures could breach the cap), or could force the stimulus measures to be offset by other cuts that withdraw needed cash from the economy. The cap could thereby interfere with sound fiscal policy.

Third, despite the wide-ranging nature of the entitlement cap proposal, it would exempt an entire class of entitlement programs — those that Federal Reserve Board Chairman Alan Greenspan has called “tax entitlements” and that the Joint Committee on Taxation refers to as “tax expenditures.” These are the many hundreds of billions of dollars of entitlement-style subsidies that are delivered through the tax code, via special tax breaks, write-offs, preferences, shelters, and the like. Whereas middle-class and low-income Americans receive the bulk of their government benefits through program entitlements, wealthy individuals and corporations receive the majority of their government benefits and subsidies through tax entitlements. By exempting tax entitlements from the cap, the proposal effectively favors affluent individuals and powerful corporations over ordinary Americans.

Finally, despite the severe cuts that the Hensarling proposal would require, the proposal would not necessarily result in deficit reduction. The Hensarling bill would not place any limitations, or any form of fiscal discipline, on tax cuts. To the contrary, the bill would make permanent tax cuts easier to pass.[2] As a result, nothing in the bill would prevent deep cuts in entitlement benefits for the elderly, people with disabilities, veterans, low-income children, and others from being used to make room in the budget for further rounds of tax cuts for affluent Americans and special interests with high-priced lobbyists.

|

Factors Beyond Policymakers’

Control that Could Cause the The following are some of the uncontrollable factors that could boost entitlement expenditures and thereby require even deeper cuts in entitlement programs. Most of these factors would increase costs only on a temporary basis. But all entitlement reductions made as a result of automatic cuts would be permanent. Entitlement costs

would rise farther beyond permitted levels — and deeper cuts consequently

would be required — if:

|

In fact, establishment of an entitlement cap could doom chances to reach a “grand bargain” in which all parts of the budget are placed on the table and major deficit-reduction is achieved through a bipartisan agreement, as occurred in 1990. Advocates of entitlement cuts would have no reason to join a grand bargain if, through an entitlement cap, they have already achieved their policy objectives. Yet history suggests that unless all parts of the budget — including revenues, entitlements, and discretionary programs — are on the table and a spirit of “shared sacrifice” is invoked, large-scale deficit reduction is unlikely to be achieved.

Click here to view full report.

End Notes:

[1] The Hensarling legislation, H.R. 2290, addresses many aspects of the budget process. This analysis examines only the provision capping entitlements, which is similar, but not identical, to the entitlement cap contained in a proposal that Rep. Hensarling offered in June 2004.

[2] The Hensarling bill includes a provision repealing the Senate rule that bars budget reconciliation bills from increasing deficits in years beyond the years that the reconciliation directive covers. This rule is a central reason why the 2001 reconciliation legislation had to include sunsets on its tax cuts, rather than making them permanent. Repeal of this rule would make permanent tax cuts easier to pass.