June 29, 2005

IN A LEAGUE OF THEIR OWN:

Colorado’s TABOR And Ohio’s Proposal Are More Restrictive Than Other Limits

By David Bradley and Iris Lav

| PDF of full report |

| If you cannot access the files through the links, right-click on the underlined text, click "Save Link As," download to your directory, and open the document in Adobe Acrobat Reader. |

A “tax and expenditure limit,” or “TEL,” is a general term used to describe a provision in state law that restricts the growth of either revenue or spending at the state and/or local level. Since the late 1970s, some 29 states have adopted some limit on revenue, spending, or both. But TELs vary greatly from one another with respect to their impact on state finances. Some TELs restrict the ability of a state to provide an adequate level of services to its residents; others allow a reasonable level of flexibility to provide services as needed. There is one TEL, however, that is far more restrictive than all the rest. It is called TABOR, and it has been in effect in Colorado since 1992.

Colorado’s Taxpayer’s Bill of Rights, or TABOR differs significantly from the majority of TELs in other states. It arguably has resulted in far greater deterioration of services in Colorado than has occurred as a result of a TEL in any other state. TABOR has three core elements.

- Colorado’s TABOR is in the state constitution. It thus can only be changed by waging a costly campaign for voter approval on the ballot.

Some 15 other states have constitutional TELs. In none of the other 15 states, however, is a constitutional TEL found in combination with the other two factors described below that make a TEL particularly stringent.

- Colorado’s TABOR limits growth of government services to a formula of inflation plus population growth. This formula virtually guarantees that state services will have to be cut every year, because inflation and general population growth do not adequately measure the increase in the cost of what government buys, including health care, education, and services to the growing elderly population and populations with special needs.

Three other states have an inflation plus population formula in their TELs, but those formulas do not operate in the same way as Colorado’s. In one of the states the formula applies to the proposed budget but not to the enacted budget. In another state, major portions of the budget are exempt from the limit. In the third state the formula is applied in a way that provides ample room under the limit for needed expenditures. Only Colorado applies the strict formula to virtually the entirety of the enacted budget.

The Definition of “TABOR”

TABOR is a state tax and expenditure limit that includes the following elements:

It is a constitutional amendment It restricts revenue or expenditure growth to the sum of inflation plus population change It requires voter approval to override the revenue or spending limits

- Colorado requires a vote of the people to override the TABOR limit temporarily in response to unusual circumstance. This cumbersome process greatly limits the flexibility of the governor and legislature to adapt to changing fiscal circumstances.

No other state requires voter approval to override its TEL temporarily in response to a problem. In all other states, a majority or supermajority of the legislature can override the TEL.

Colorado’s tax and expenditure limit is the only one in the country with the combination of the most restrictive type of legal authority, growth formula, and provisions for a temporary override of the limit. Any proposed tax and expenditure limit that includes these three elements is a “TABOR,” because it will impair the ability of a state and localities to provide an adequate level of service to its residents. Other characteristics, such as the manner in which “surplus” revenues are refunded, whether a rainy day fund is required, whether the TEL applies to revenues or expenditures, and the portion of the budget covered by the TEL are of lesser importance than the three key dimensions described above.

Placing TABOR in Context

The following sections compare Colorado’s TABOR to the 28 other tax and expenditure limits in the country, based on the three key elements discussed above — legal authority, growth formula, and override mechanism (see box “The Definition of TABOR”). As the only constitutional TEL that restricts budget growth to population changes plus inflation and creates high barriers to override those limits, Colorado’s TABOR is in a league of its own.

A TEL in the Constitution

Constitutional tax and spending limits are restrictive and inflexible. Placing a restrictive TEL in a state constitution is a priority of individuals and organizations that seek to shrink government precisely because it makes change difficult. (See section “Proponents of TABOR” below.) While states prescribe different routes for amending their constitutions, all are arduous. In most states amendments must be passed by the legislature, and some states require passage in more than one session or by more than a simple majority.

Colorado’s TABOR Has Hurt Health Care and Education

Colorado’s TABOR, which was passed in 1992, has contributed to a decline in public services in Colorado. Education and health services were particularly hard hit.

The percentage of low-income children lacking health insurance in Colorado rose from 15 percent in 1991-92 to 27 percent in 2002-03. During the same period, the national proportion of low-income children lacking health insurance fell from 21 percent to 19 percent. Reflecting funding cuts, Colorado’s ranking on access to adequate prenatal care dropped from 23rd in 1992 to 48th in 2002. Colorado’s ranking for on-time vaccination of children fell from 20th in 1995 to 50th in 2003. The percentage of Coloradoans with no health insurance rose from 12.7 percent in 1992 to 15.6 percent in 2001, dropping its ranking from 24th to 36th. In 2000-01, Colorado ranked 49th in current expenditures per $1,000 of personal income for public K-12 schools. K-12 education spending per pupil in Colorado fell by more than $300 compared to the national average from 1992 to 2000. Colorado’s ranking for average teacher pay compared to private-sector earnings fell from 30th in 1992 to 50th in 2001.a Adjusted for student enrollment and inflation, the state’s contribution to higher education in 2004-05 was 38 percent below its level in 1991-92. Colorado’s ranking for expenditures on higher education relative to personal income dropped from 35th in 1992 to 48th in 2004. aIn 2000, voters put another formula into the constitution — Amendment 23 — to ensure somewhat higher education funding. Increasing funding for one program, however, places additional pressure on the rest of the budget due to TABOR’s restrictive limits.

Sources: CBPP analysis of data from the U.S. Bureau of the Census Current Population Survey; National Center for Health Statistics; National Center for Education Statistics; Bureau of Economic Analysis; National Education Association; Colorado Joint Budget Committee; and Colorado Legislative Council.

Once passed by the legislature, the amendment must be placed on the ballot for a popular vote. Some states require a supermajority of voters to approve the amendment. The initiative process is an alternative path in some states, whereby citizens can collect signatures to put a constitutional amendment on the ballot. In all cases, however, the success or failure of the amendment on the ballot may depend on the ability of proponents or opponents to finance polling, advertising and other activities that characterize a modern campaign.

Pro-TABOR advocates argue that constitutional TELs prevent legislators from weakening the restrictiveness of a limit or changing the base to which the limit applies. This is another way of saying that constitutional limits severely curb the flexibility of legislators and prevent them from adapting quickly to changing circumstances.

Of the 29 states with TELs, 16 have limits in the constitution. (See Table 1.)

While it is not uncommon for states to place TELs in their constitutions, it is uncommon to embed the other

TABLE 1

LEGAL AUTHORITYConstitutional

Statutory

16

13

Alaska

Idaho

Arizona

Indiana

California

Iowa

Colorado

Maine

Connecticut

Massachusetts

Delaware

Mississippi

Florida

Montana

Hawaii

Nevada

Louisiana

New Jersey

Michigan

North Carolina

Missouri

Oregon

Oklahoma

Utah

Rhode Island

Washington

South Carolina

Tennessee

Texas

elements of TABOR — a population-plus-inflation growth formula and strict limits on waiver provisions — within a state constitutional TEL.

A Population Growth Plus Inflation Formula

Limiting state revenue or spending growth to changes in population plus inflation shrinks government over time and severely limits the scope of government. While no existing measure of inflation adequately captures the cost structure facing governments, the inflation factor TABOR proponents use is particularly insidious. The Consumer Price Index (CPI-U) is designed to measure average cost increases for a basket of goods for urban consumers, not for state governments. Health care and education spending comprise a majority of state budgets and costs in health care and education tend to rise much faster than the overall CPI-U.[1] The population factor also is flawed, because certain subpopulations that require additional public services, such as the elderly, tend to grow faster than the overall population. Of the 29 states with TELs, only four — Alaska, Colorado, Nevada, and Utah — use population-plus-inflation as the growth formula to limit state spending or revenues. (See Table 2.)

Moreover, in the three states other than Colorado that use the inflation plus population factor, it is not applied in the same way as it is in Colorado. In Alaska, the limit was set to allow state government to grow from a specific dollar amount in 1982 ($2.5 billion) and state spending remains far below that inflation-adjusted level. In Nevada, the population-plus-inflation formula applies only to the governor’s proposed general fund expenditures, and not to the budget enacted by the legislature. Thus the formula does not create a binding limit on actual expenditures. In Utah, the legislature in 2004 changed its spending cap formula to inflation and population growth from the existing combination of inflation, population growth, and personal income growth. But the Utah legislature also exempted from the cap spending on public education and transportation.

Moreover, Nevada and Utah are statutory limits and so can be amended by the legislature at any time. In Colorado, by contrast, the formula applies to the revenues that support virtually the entire state government, and is binding for the enacted budget.[2]

TABLE 2

GROWTH FORMULAPopulation + Inflation

Personal Income

Other

4

19

6

Alaska

Arizona

Delaware

Colorado

California

Iowa

Nevada

Connecticut

Massachusetts

Utah

Florida

Mississippi

Hawaii

Oklahoma

Idaho

Rhode Island

Indiana

Louisiana

Maine

Michigan

Missouri

Montana

New Jersey

North Carolina

Oregon

South Carolina

Tennessee

Texas

Washington

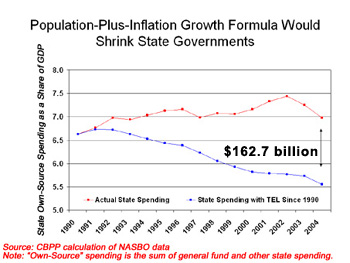

Figure 1 shows how an inflation plus population growth formula shrinks government over time.

If a TABOR been in effect since 1990 in all states, total state own-source spending would have been $162.7 billion lower than actual expenditures in fiscal year 2004.

A Restrictive Override Mechanism

Colorado is the only state that requires voter approval to temporarily override TABOR provisions. Other states allow either a majority or supermajority of the legislature to override their limits. (See Table 3.)

The Colorado legislature is constitutionally prohibited from spending above the TABOR limits even if revenues exist to fund such spending. If the state needs to spend revenues above the limit, such as in the current situation in which the strict TABOR limit is preventing the state from recovering from the economic downturn, a vote of the people is required. Similarly, if there is a revenue shortfall or other fiscal crisis such

as occurred in 2001, Colorado legislators cannot raise taxes without voter approval; the only option for budget adjustment is expenditure reductions.[3]As noted above, obtaining voter approval can be a difficult and expensive process. Given the cost of campaigns and advertising and the complexity of the issues involved, the outcome may reflect something other than the true public sentiment. Moreover, in times of crisis when legislatures may need to act quickly to raise revenue, voter approval is an impediment to legislators’ ability to respond.

Figure 1

The Blackwell Proposal in Ohio is a TABOR

Citizens for Tax Reform (CTR), is attempting to place an expenditure limitation proposal on the ballot in November 2005. Ohio Secretary of State Ken Blackwell, head of CTR, has recently denied that his group’s expenditure limit is fundamentally the same as Colorado’s TABOR. Secretary Blackwell has described his expenditure limit as “substantially” different than Colorado’s and has claimed that comparison to Colorado is “silly on its face” and “unfair.” Nevertheless, the proposed Blackwell amendment shares the three key characteristics of Colorado’s TABOR. Thus concerns that the harm TABOR has done in Colorado will be imported to Ohio are justified.

Blackwell Claim:

The Ohio proposal limits spending, not revenue.[4]Reality: In a state with a balanced budget requirement, in which expenditures must be lower than or equal to revenues, it makes little difference whether it is revenues or expenditures that are capped. Under a revenue limit, revenues above the limit cannot be spent and thus constitute a limit on expenditures. An expenditure limit directly limits spending; any additional revenues a state collects cannot be spent. The effect is the same. Ohio has a balanced budget requirement, and so would fare the same under a revenue or expenditure limit. [5]

TABLE 3

OVERRIDE MECHANISMVoter Approval

Supermajority

Majority

1

17

11

Colorado

Alaska

Idaho

Arizona

Indiana

California

Iowa

Connecticut

Maine

Delaware

Massachusetts

Florida

Mississippi

Hawaii

Nevada*

Louisiana

North Carolina

Michigan

Rhode Island

Missouri

Tennessee

Montana

Texas

New Jersey

Oklahoma

Oregon

South Carolina

Utah

Washington**

*Override mechanism is not relevant since limit applies to recommended budget and is non-binding.

**State expenditure limit can be exceeded by a two-thirds vote of the legislature following declaration of an emergency, which is defined as “limited to natural disasters.” This presumably rules out “economic emergencies” but the expenditure limit is statutory and can be altered by the legislature, as occurred in 2005.

Blackwell Claim: The Ohio proposal gives some additional flexibility as compared to Colorado because it limits the growth of state spending to the greater of state population change plus inflation (as measured by the Midwest CPI-U) or 3.5 percent.[6]

Reality: Blackwell’s TABOR allows growth of at least 3.5 percent each year. This is slightly different than Colorado’s TABOR, which has no minimum guaranteed growth rate. But the 3.5 percent minimum in Ohio would make only a marginal difference in the degree to which expenditures would be restricted; the guarantee is still lower than the growth required to maintain health, education, public safety, and other critical state programs from year to year.

The difference the 3.5 percent guarantee would make can be understood by analyzing the effect a TABOR limit would have with and without the guarantee if TABOR had been approved in Ohio in 1994. Without the 3.5 percent minimum growth factor, Ohio would have had to cut a cumulative total of $24.3 billion from state spending from 1994 to 2004; with Blackwell’s proposal, cumulative spending cuts would have totaled $19.3 billion over the same period. Either formula would have caused deep and painful cuts in Ohio.[7]

Blackwell Claim: The Ohio proposal retains significant resources in a “rainy day” fund.[8]

Legal Authority Growth Formula Override Mechanism TABOR

Constitutional Population + Inflation Voter Approval Blackwell Proposal Constitutional Population + Inflation or 3.5% (whichever is greater) Voter Approval Reality: By requiring deposits into a budget stabilization fund, the Ohio proposal is an improvement over Colorado’s TABOR. A robust budget stabilization fund is sound fiscal policy and would help Ohio weather economic downturns. The establishment of a budget stabilization fund, however, does not alter the fundamental effect of Blackwell’s TABOR proposal — the shrinking of government. And many states maintain strong rainy day funds without a TABOR; there is no need to approve a TABOR just to have a rainy day fund.

Proponents of TABOR

An important clue that Colorado’s TABOR is different than all other TELs may be found in the words of its strongest proponents. Rather than pushing tax and expenditure limits in general, leading conservative ideologues favor the restrictive Colorado-model TABOR.

- Grover Norquist, president of Americans for Tax Reform, has called Colorado’s TABOR the “holy grail” of state fiscal policy.

- In a February 28, 2005 editorial The Wall Street Journal noted, “States have been adopting tax and spending limits since the 1970s and 28 now have them on the books. Some are more restrictive than others, but Colorado's Taxpayer's Bill of Rights (also known as Tabor), passed in 1992, is considered the gold standard.” (Emphasis added.)

Barry Poulson of The Americans for Prosperity Foundation [an organization dedicated to propagating TABORs around the country frequently argues that TABOR has several “essential features” — it is constitutional, it limits government growth to population plus inflation, it requires voter approval for any tax increase, and it requires surplus revenue to be returned to taxpayers.[9]

The main national proponents of the Colorado model — the Cato Institute, Americans for Prosperity Foundation, and the American Legislative Exchange Council — agree on the following requirements for creating a stringent TEL: constitutional, population change plus inflation growth formula, and voter approval or a legislative supermajority to override the limits.[10]

[1] For a detailed analysis of the problems with the population change plus inflation formula, see David H. Bradley, Nicholas Johnson, and Iris J. Lav, The Flawed “Population Plus Inflation” Formula; Why TABOR’s Growth Formula Doesn’t Work, Center on Budget and Policy Priorities, January 2005.

[2] In Colorado, the formula allows growth by inflation plus population growth from the amount of revenues in the previous year. During economic downturns, when revenue growth slows or declines, this becomes a severe limit that impedes recovery from the downturn. Some but not all of the TABORs proposed in other states have this feature.

[3] While the legislature (with a two-thirds supermajority) can raise taxes without voter approval in an “emergency”, the definition of an emergency explicitly excludes economic conditions, revenue shortfalls, and salary or benefit increases. In practice, then, barring a non-economic catastrophic disaster, the Colorado legislature cannot waive the TABOR restrictions without voter approval.

[4] “New Coalition Opposes Spending Amendment,” Plain Dealer, April 20, 2005.

[5] At least some pro-TABOR forces have a preference for expenditure limits because they believe they are stricter. For example, the Cato Institute has argued, “the ideal TEL would cap spending rather than revenue or taxes.”Dean Stansel, op cit. While the operation of an expenditure limit is more direct, there is little difference between expenditure and revenue limits.

[6] “Plan to Limit Spending Criticized,” The Columbus Dispatch, April 20, 2005.

[7] See David Bradley and Iris J. Lav, A State of Decline: What a TABOR Would Mean for Ohio, Center on Budget and Policy Priorities, April 2005.

[8] “New Coalition Opposes Spending Amendment,” Plain Dealer, April 20, 2005.

[9] See, for example, Barry Poulson, A Taxpayer’s Bill of Rights (TABOR) for Kansas, Americans for Prosperity Foundation, December 2004.

[10] Source: Dean Stansel, Taming Leviathan: Are Tax and Spending Limits the Answer?, Cato Institute, Policy Analysis No. 213; Barry Poulson, The Next Generation of Tax and Expenditure Limits, Americans For Prosperity Foundation, http://www.americansforprosperity.org/news/spend_0040512b.html