HOUSE

BILL ADDS $69 BILLION IN DEFICIT-FINANCED TAX CUTS BY EXTENDING

CHILD TAX

CREDIT TO FAMILIES WITH INCOMES UP TO ABOUT $300,000

Bill Includes Temporary

Token for Low-Income Families, Alongside Large

New Permanent Tax Cuts for

Higher-income Families, Including Members of Congress

by

Robert Greenstein

|

PDF of

report |

|

| If you cannot access the files through the links, right-click on the underlined text, click "Save Link As," download to your directory, and open the document in Adobe Acrobat Reader. |

The child tax credit bill that the House of

Representatives will consider this week greatly expands the tax credit for

families in the $110,000 to $300,000 range, ballooning the bill’s cost to $228

billion through 2014, according to the official Joint Tax Committee estimate,

and to $213 billion according to the

- Under current law, married families with incomes up to $110,000 receive the full tax credit of $1,000 per child. Married families with two children who have incomes between $110,000 and $149,000 receive a partial tax credit (i.e., a credit of less than $1,000 per child).

- Families with two children that have incomes above $149,000 do not qualify for the credit but already receive some of the largest tax-cut benefits provided by the other tax cuts enacted over the past three years, including the reductions in upper-bracket tax rates and reductions in capital gains taxes, dividend taxes and the estate tax. Moreover, families at these income levels do not need government assistance through the child tax credit to meet the basic costs of providing for their children.

- The House bill, however, would more than double the income thresholds for the child tax credit, raising from $110,000 to $250,000 the income level up to which the full credit of $1,000 per child is provided to married filers, effective in 2004.[1] Married families with two children and incomes between $250,000 and $289,000 would receive a partial child credit. If a family has three children, it would receive a partial credit until its income reaches $309,000.

|

Number of Children |

Current Law |

House Bill |

||

|

Credit begins to phase out at incomes of:* |

Credit phases out completely at: |

Credit begins to phase out at incomes of:* |

Credit phases out completely at: |

|

|

1 |

$110,000 |

$129,000 |

$250,000 |

$269,000 |

|

2 |

$110,000 |

$149,000 |

$250,000 |

$289,000 |

|

3 |

$110,000 |

$169,000 |

$250,000 |

$309,000 |

|

* Credit is reduced by $50 for each $1,000 of income above this threshold level |

||||

- The

- Tax

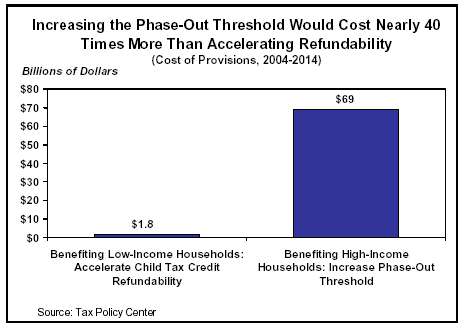

- The House bill does accelerate by one year, to 2004, an increase in the low-income component of the child tax credit that is scheduled to take effect in 2005. This very modest provision, which applies only to low-income families with earnings over $10,750 (families with earnings below $10,750 are not eligible for the credit), would provide $1.8 billion in additional tax benefits to these families. As noted, the extension of the child tax credit to higher-income families costs $69 billion through 2014, or 38 times more.

- None of the bill’s costs would be offset; they would be financed entirely through higher deficits. Using the Joint Tax Committee’s cost estimate, the bill would add $279 billion to deficits through 2014, including the increased interest payments on the debt that the bill would generate.

- Raising the income threshold for the full credit from $110,000 to $250,000 would not increase economic efficiency or economic incentives. The principal economic effects of expanding the child credit to higher-income families would be the adverse effects of the larger budget deficits that the proposal would engender.

|

House Bill Extends

Child Credit Tax Cut to Members of Congress While The House child tax credit bill would give a substantial new tax break to most Members of Congress with children.

* A married family with $15,000 in earnings in 2004 would receive a tax cut equal to 15 percent of the amount by which its earnings exceed $10,750. Such a family would receive a child tax credit of $637.50 (which is 15 percent of $4,250, the amount by which the family’s earnings exceed $10,750). |

Low-income Families to Receive Small Temporary

Gain,

but Likely to be Harmed Over Time

Some media accounts last week reported that the House bill would make the child tax credit available to more upper-income and more lower-income families. This claim is not correct: while the bill more than doubles the income threshold at the top to extend the credit to more high-income families, it does not make additional low-income families eligible for the credit.[2]

|

Table 2 |

|||

|

Income |

Current Child Credit |

Credit Under House Bill |

Increase Per Child |

|

$12,000 |

$125 |

$187.50 |

$31.25 |

|

$15,000 |

$425 |

$637.50 |

$106.25 |

|

$20,000 |

$925 |

$1,387.50 |

$231.25 |

As noted, the bill accelerates by one year an increase in the size of the low-income component of the child tax credit scheduled to take effect in 2005.[3] Low-income families that qualify for the child tax credit would receive a modestly larger credit in 2004 than they otherwise would get. This change would provide an additional benefit only in 2004, with the increased benefit averaging $150 per child for the low-income families that qualify for it.

Working-poor families with a parent who works full time throughout the year at the minimum wage would not qualify.[4] They would remain ineligible for the child tax credit, since families must have earnings above $10,750 to qualify. By contrast, families in the $150,000 to $250,000 range would become eligible for the full credit. They would receive an additional tax benefit of $1,000 per child every year in perpetuity, starting with 2004.

-

Between now and 2014, the low-income families with two children that would benefit from the acceleration of the low-income child tax credit provision would receive an additional $300, on average, as a result of the acceleration. (Some of these families also would benefit from the extension of the $1,000 maximum credit amount beyond

-

By comparison, families with two children that make between $150,000 and $250,000 would receive an additional $22,000 in tax cuts through 2014 as a result of the increase in the income threshold for the credit. ($2,000 a year for the 11 years from 2004 through 2014 equals $22,000.)

|

Table 3 |

||

|

For a Married Family with Two Children |

||

|

Family has Minimum-Wage Earnings |

Low-income Family with Earnings Above Minimum Wage Level (average increase in tax benefits) |

Families in $150,000-$250,000 Range, Including Many Members of Congress |

|

$0 |

$300 |

$22,000 |

Overall, the combined long-term effect of accelerating the increase in the credit for low-income working families by one year while raising to $250,000 the income level up to which families may receive the full credit would likely be harmful for low-income children and families. These families would receive no ongoing gains from the acceleration, and the $69 billion in increased costs through 2014 from extending the child tax credit to higher-income families would further enlarge budget deficits that already threaten to reach economically unsustainable levels in the decades ahead. Because of the unsustainably large deficits that loom, the cost of this new tax cut for higher-income families would eventually have to be offset. The odds are substantial that when offsetting savings ultimately were produced, part of those savings would come from reductions in programs that assist low-income families, since such families are a weak political constituency.

End Notes:

[1] For single-parent families, the income threshold would be raised from $75,000 to $125,000.

[2] A small exception to this statement is that a change the bill would make regarding the treatment of combat pay in the calculation of a family’s child credit could make a very small number of low-income families eligible for the credit.

[3] Currently, the child tax credit for families with incomes too low to owe income tax equals 10 percent of the amount by which a family’s earnings exceed $10,750, up to a maximum of $1,000 per child. In 2005, the 10 percent factor is slated to rise to 15 percent; the House bill would accelerate this increase into 2004. Under the bill, the child tax credit in 2004 would equal 15 percent (rather than 10 percent) of the amount by which a family’s earnings exceed $10,750.

[4] Depending on the calculation used, full time minimum wage earnings equal either $10,300 ($5.15 an hour for 40 hours a week for 50 weeks a year) or $10,712 (if the computation is made for 52 weeks rather than 50).