|

Revised July 6, 2007

INTRODUCTION TO THE HOUSING VOUCHER PROGRAM

Introduction

This analysis provides an introduction to the “Section 8” Housing Choice Voucher Program, covering the following key questions:

- What is the housing voucher program? Created in the 1970s, the Section 8 housing voucher program has become the dominant form of federal housing assistance. Low-income families use vouchers to help pay for housing that they find in the private market. The program is federally funded, but vouchers are distributed by a network of 2,400 local, state, and regional housing agencies.

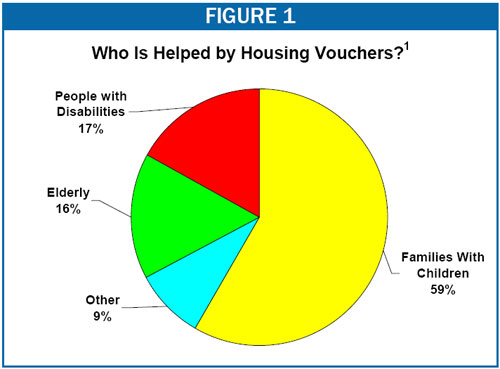

- Who is eligible for vouchers? Vouchers are a critical form of assistance for low-income families with children, the elderly, and people with disabilities. Federal rules ensure that vouchers are targeted at the families who need them most.

- How does a family use a voucher? Once a family receives a voucher, it has at least 60 days to find housing. Due to shortages of moderately priced housing and some landlords’ reluctance to accept vouchers, not every family is able to use its voucher.

- How much rent do vouchers cover? A family with a voucher is generally required to contribute 30 percent of its income for rent and utilities. The voucher then pays the rest of those costs, up to a limit (called a “payment standard”) set by the housing agency.

- Are vouchers used only to help cover rental costs? No. Vouchers are sometimes used to help with mortgage payments, enabling low-income families to purchase homes. Also, up to 20 percent of voucher funds can be used for subsidies — called “project-based” vouchers — that are tied to a particular building rather than a particular family and thus can help pay for the construction or rehabilitation of housing for low-income families.

- How are vouchers allocated to state and local housing agencies? Each agency has a cap on the number of vouchers it is authorized to administer. An agency’s number of “authorized vouchers” is essentially the sum of the vouchers the agency has been awarded since the start of the voucher program. Each year, Congress provides some new vouchers in addition to renewing existing ones. Since 2003, all new vouchers have been “tenant-protection” vouchers, which are provided to replace either public housing that is demolished or sold or other affordable housing units that lose federal subsidies.

- How are vouchers funded? The amount of voucher funding most state or local housing agencies received in 2007 is based on the number of an agency’s authorized vouchers that were in use in 2006 and the actual cost of those vouchers, adjusted for inflation and several other factors. Funding for new vouchers and administrative costs is provided separately. Agencies facing certain special circumstances (such as some agencies affected by Hurricanes Katrina and Rita or participating in the Moving-to-Work demonstration) are funded under different formulas.

- How effective are vouchers? Research has shown that vouchers are more cost-effective than federal programs that build affordable housing for low-income households. Vouchers have been found to sharply reduce homelessness and housing instability — both of which have been linked to a variety of developmental and health problems in children — and to help families move to lower-poverty neighborhoods with better schools and higher rates of employment.

What Is the Housing Voucher Program?

The Housing Choice Voucher Program (sometimes referred to as the “Section 8 voucher program” after the section of the U.S. Housing Act that authorizes it) is the largest federal low-income housing assistance program. Families who are awarded vouchers use them to help pay the cost of renting housing on the open market. Because most vouchers are provided to particular tenants to live where they choose, they are often referred to as “tenant-based” assistance. Vouchers can also be used to help families buy homes, or tied to particular affordable-housing developments.

The voucher program is administered at the federal level by the Department of Housing and Urban Development (HUD). At the local level, the program is run by approximately 2,400 local, state, and regional housing agencies, known collectively as public housing agencies (PHAs). Many of these are independent public authorities, while others are part of city, county, or state governments and thus are directly under the supervision of elected officials. (Twenty-five housing agencies, administering about 10 percent of the total number of vouchers, participate in the Moving-to-Work (MTW) demonstration. MTW, which was authorized by Congress in 1996, permits HUD to enter into temporary agreements with a limited number of housing agencies to waive many of the federal rules governing the voucher and public housing programs.)

The Section 8 program was established in 1974 during the Nixon-Ford Administration. Major changes to the tenant-based portion of the program were made by legislation passed in 1983, 1987, and 1998. As part of the 1998 legislation, Congress merged the two previous components of the tenant-based Section 8 program — certificates and vouchers — into a single housing program.

The voucher program currently assists about 1.95 million households.[2] It is the only federal housing program primarily serving poor families that has grown as needs have grown over the last 20 years. The emergence of vouchers as the centerpiece of federal low-income housing policy reflects a major shift during the last 30 years toward more market-based housing subsidies. Previously, the federal government had focused on supporting the construction of public housing or on subsidizing affordable private housing with project-based subsidies.

Housing vouchers are not an entitlement benefit. Because of funding limitations, only one in four households that are eligible for vouchers receive any form of federal housing assistance.[3] Most areas have long and growing waiting lists for vouchers, and many housing agencies have even stopped accepting new applications because of the size of the backlog.

The need for housing assistance is very great. HUD’s most recent analysis of Census data indicates that in 2005, 6.5 million low-income renter households that did not receive housing assistance had “severe housing problems,” which means they either paid more than half of their income for rent and utilities or lived in severely substandard rental housing. This number increased by 20 percent between 2001 and 2005. High housing-cost burdens contribute to housing instability and homelessness, which in turn have cascading effects on the well-being of children and other family members. Working families are among those who struggle the most to afford housing. A majority of the low-income families without housing assistance who face severe housing problems (excluding those who get Social Security) are working families.[4]

Who Is Eligible for Vouchers?

Income eligibility limits for the voucher program are set as percentages of the median income in the local area. (Each year HUD estimates the median income for households of different sizes in every metropolitan area and rural county in the nation.) State and local housing agencies have substantial flexibility to determine which families they will serve, and are permitted to establish admission preferences based on household characteristics (such as preferences for working families or families that live in particular areas) or on housing needs such as homelessness.

- Income limits. Each housing agency must set the overall income cap for families admitted to its voucher program between 50 percent and 80 percent of the local area median income. (Nationally for a family of three, 50 percent of median income is $26,600 and 80 percent of median income is $42,500.) Technically, a housing agency may only set the overall income cap above 50 percent of area median income if it states a reason for doing so in its annual plan for the voucher program, but this requirement does little to restrict agencies’ flexibility.

Income limits are only applied at the time a family enters the voucher program, so a family can continue to use its voucher if its income later rises above the limit. The amount of a voucher subsidy falls as a family’s income rises, however, and in practice a family’s subsidy generally fades to zero before (or soon after) its income reaches 80 percent of area median income.

- Targeting to the neediest families. Housing agencies are required to ensure that 75 percent of households newly admitted to the voucher program each year have incomes at or below 30 percent of the area median. (Nationally, 30 percent of median income is $15,900 for a family of three, close to the poverty line.) As with income limits, the targeting requirement is only applied when families are first admitted to the voucher program.

HUD refers to households with incomes up to 80 percent of the area median as low-income households, those with incomes up to 50 percent of the area median as very low-income households, and those with incomes up to 30 percent of the area median as extremely low-income households.

How Does a Family Use a Voucher to Obtain Housing?

A family can apply for a voucher at any of the 2,400 agencies that administers the voucher program. Vouchers become available when the agency receives new vouchers or families leave the program.[5] Waiting times are frequently very long; in 2000 the average wait for a voucher was 28 months. A 2004 study found that 40 percent of housing agencies examined had waiting lists that were so long that the lists had been closed to new applicants.[6]

A family that receives a voucher may use it either to help pay the rent of its current unit or to rent a different unit. In either case, the family must lease a unit with the voucher within a fixed period set by the housing agency (agencies must give voucher holders at least 60 days but can give them a longer period) or the family will lose the voucher.

Once a family identifies a unit, the housing agency must inspect the unit to determine that it meets the voucher program’s housing quality standards. In addition, the agency must certify that the rent is “reasonable” — that is, consistent with market rents for similar units in the local area. The agency then signs a contract with the landlord and makes monthly subsidy payments directly to the landlord. The landlord and the family also sign a lease agreement.

A family may use its voucher in any part of the country where there is a voucher program, except that an agency issuing a voucher to a family that lived outside the agency’s jurisdiction when it applied for assistance can require that the family use the voucher within the agency’s jurisdiction for one year. If a family exercises the option (referred to as portability) to use a voucher to move beyond the issuing agency’s jurisdiction, the agency in the community to which the family moves takes on administrative tasks such as inspecting apartments and determining that rents are reasonable. This receiving agency then bills the issuing agency for the cost of the voucher, unless the receiving agency chooses to “absorb” the voucher into its own program.

Landlords are under no obligation to rent to families with vouchers, although landlords who receive Low-Income Housing Tax Credits or some other federal subsidies are forbidden to discriminate against a family because it has a voucher. (Some states and localities also prohibit unsubsidized landlords from discriminating against voucher holders.) Some families are not able to use their vouchers within the allowed time period, for reasons such as a shortage of moderately priced housing and the reluctance of some landlords to accept vouchers. If this occurs, the family loses the voucher and the housing agency awards it to a different family.

Studies have found that the proportion of voucher holders who are able to use their vouchers — known as the success rate — fell from 81 percent in the early 1990s to 69 percent in 2000. This decline appears to have reflected the tight housing markets in many areas at the time of the latter survey; no subsequent national data are available.

The percentage of a housing agency’s vouchers that are in use is referred to as the agency’s utilization rate. Nationally, the voucher utilization rate in 2006 was about 92 percent, a decline from the 2003-2004 rate of 98 percent.[7] Housing agencies can attain a utilization rate that is well above their success rate by “overissuing” vouchers, just as airlines over-book flights. For example, if one out of every five families typically is unable to use its voucher, the agency can issue five vouchers for every four vouchers that it has the funds to support. Housing agencies must be able, however, to cover costs if a higher-than-expected share of families use their vouchers successfully. In recent years, erosion of agencies’ reserve funds and other policy changes have made it difficult for many agencies to overissue as efficiently as they previously had.

How Much Rent Do Vouchers Cover?

The amount of rent a voucher can cover is capped by a payment standard set by the housing agency. An agency is allowed to set the payment standard anywhere between 90 percent and 110 percent of the fair market rent, which is HUD’s estimate of the amount needed to cover the rent and utility costs of moderately priced housing units in the area. HUD has the authority to allow agencies to set payment standards outside this range, but it has allowed increases only rarely in the past several years.

HUD sets fair market rents annually in each metropolitan area and non-metropolitan county for units with different numbers of bedrooms. In most areas, the fair market rent is set at an amount sufficient to pay rent and utility costs for 40 percent of the recently rented units in the area, excluding new units. In 28 metropolitan areas where HUD has determined that these “40th percentile rents” are insufficient to enable voucher holders to rent housing outside a few low-cost neighborhoods, HUD sets the fair market rent at the 50th percentile instead.

The amount that a voucher pays is based on: (1) the payment standard, (2) the actual rent and utility costs of the housing unit, and (3) the family’s annual “adjusted income,” which includes deductions for each child as well as child care costs. (Households may also have costs of assistance for a person with a disability deducted. In addition, households in which the head or spouse is elderly or has a disability receive a special standard deduction, and may have unreimbursed medical expenses deducted as well.)

- If a family rents a unit with rent and utility costs that exactly equal the payment standard, the voucher pays the landlord the payment standard minus 30 percent of the family’s adjusted income, and the family pays the rest. (Since the early 1980s, federal policy has set 30 percent of income as the maximum a low-income family should devote to housing, given other demands on family budgets; many experts think this standard is too high for the lowest-income families.) In rare cases where families have high child care or medical deductions, they will be required to contribute 10 percent of their gross income if that amount is higher than 30 percent of their adjusted income.

- If rent and utility costs are below the payment standard, the family still pays 30 percent of its adjusted income and the voucher covers the remaining cost.

- If rent and utility costs exceed the payment standard, the voucher covers the payment standard minus 30 percent of the family’s income and the family pays the rest. As a result, a significant share of families with vouchers pay more than 30 percent of their income for housing. However, new participants in the program and families moving to new units are not allowed to rent units that would cause them to pay more than 40 percent of their adjusted income for housing.

- If the housing agency has established a minimum rent (which may be up to $50 per month), the family is required to pay the minimum rent regardless of how big a share of its adjusted income the minimum rent constitutes, as long as rent and utility costs do not exceed the payment standard. If these costs do exceed the payment standard and the family’s share of the costs is more than 40 percent of its adjusted income, the voucher may not be used to rent that particular unit.

In the case of apartments with tenant-paid utilities, the amount of utility costs a voucher covers is determined by the local utility allowance (set by the housing agency based on typical costs in the area) rather than by the voucher holder’s actual costs. Typically, the family pays its own bills directly to the utility company. The agency then deducts the utility allowance from the amount of rent the family is required to pay each month.

Are Vouchers Used Only to Help Cover Rental Costs?

While the great majority of vouchers are used for tenant-based rental assistance, agencies may use some vouchers to help families purchase homes or to provide project-based rental assistance. Homeownership vouchers are used to meet mortgage payments and other ongoing homeownership costs. There is no limit to the proportion of its vouchers that an agency may use for homeownership, but agencies must still comply with the program’s regular eligibility and targeting rules. As a result, most of the agencies that have implemented voucher homeownership programs use the option to help families already receiving voucher assistance make the transition to homeownership.

An agency can also use up to 20 percent of its voucher funds for project-based vouchers, which can be used only at a designated housing development. An agency may use project-based vouchers, for example, to support construction or rehabilitation of affordable housing (by guaranteeing the developer a steady stream of revenue that can help repay debts incurred during construction), to ensure that affordable housing is available to voucher holders even when housing markets are tight, or to provide supportive housing to people with mental or physical disabilities. After one year, families living in project-based units are eligible to move to a unit of their choice using the first tenant-based voucher that becomes available. Use of project-based vouchers has increased substantially since HUD issued regulations in October 2005 clarifying the rules governing their use.

Project-based vouchers are distinct from the project-based Section 8 program, which is not funded through state and local housing agencies and is not part of the voucher program. Project-based Section 8 provides assistance to 1.3 million households through subsidy contracts with private building owners that were initially established during the 1970s and 1980s.

How Are Vouchers Allocated to State and Local Agencies?

Each agency has a cap on the number of vouchers it is authorized to administer. Over the course of a year, the average number of the agency’s vouchers actually used by families to rent housing cannot exceed the agency’s number of “authorized vouchers.” An agency’s number of authorized vouchers is not determined by any single formula. Instead, it is essentially the sum of the vouchers that the agency has been awarded since the start of the voucher program. As of January 2007, agencies were authorized to administer a total of 2,164,000 vouchers.

Each year, Congress funds some new vouchers in addition to renewing existing ones. New vouchers generally receive separate funding allocations in appropriations bills. In most years before 2003, the new vouchers issued included some incremental vouchers, which expand the number of housing subsidies available and thus reduce (or at least limit growth of) the unmet need for housing assistance. Most of these incremental vouchers were general-purpose vouchers, which HUD calls fair-share vouchers. HUD distributed these vouchers among the states based on a formula and then allocated them to housing agencies within each state on a competitive basis.

Some incremental vouchers have been “special-purpose” vouchers, designated for a particular population. For example Congress has provided mainstream vouchers to help people with disabilities live independently, and family unification vouchers to assist families where the lack of adequate housing has caused (or is threatening to cause) a child to be removed from the family. Special-purpose vouchers generally have been awarded through national competitions.

Since 2003, all new vouchers have been tenant-protection vouchers provided to replace project-based subsidized housing units, in order to prevent tenants from being made homeless and compensate communities for the loss of affordable housing resources. (Typically, the vouchers replace apartments in project-based Section 8 buildings whose owners opts to leave the program when their contract expires or apartments in public housing developments that are demolished or converted to mixed-income housing, such as through the HOPE VI program.) Because tenant-protection vouchers act as replacements for lost project-based units, they do not cause a net increase in federal housing assistance. Enhanced vouchers, a subcategory of tenant-protection vouchers, are permitted to cover somewhat higher rents than regular vouchers in order to ensure that tenants can afford to remain in buildings where rents rise after federal subsidies are eliminated.

How Are Vouchers Funded?

The voucher program is funded entirely by the federal government. The annual funding each housing agency receives for existing vouchers is often referred to as voucher renewal funding because it is technically provided through the renewal of an annual contract between HUD and the agency governing the use of voucher funds. Funding for new vouchers during the year they are first issued and administrative fees to cover agencies’ administrative costs are provided separately.

The 2007 renewal funding level for most agencies was determined by multiplying the number of the agency’s authorized vouchers that were in use during 2006 by the actual cost of those vouchers, and then adjusting for inflation and several other factors. Congress provided exceptions from this formula for three groups of agencies, which were funded based on the amount of funding they received during 2006, rather than on the actual cost of the vouchers they used during that year. These include certain agencies that were located in areas damaged by Hurricanes Katrina and Rita, that have been declared in breach of contract by HUD or placed in receivership due to mismanagement, or that spent more on their voucher programs in 2006 than they had been allocated by HUD. In addition, most agencies participating in the Moving-to-Work demonstration are funded through special formulas established by agreements between the agency and HUD.

Since 2003, Congress and HUD have repeatedly changed the voucher renewal funding formula. Largely due to the uncertainty this has created, as well as to shortfalls in federal funding at a number of agencies (since the formulas used from 2004 to 2006 were less closely linked to agencies’ actual funding needs than the 2007 formula), many agencies have been hesitant to reissue vouchers to new families from their waiting list after a voucher holder leaves the program. As a result, about 150,000 vouchers have been taken out of use since 2004.

What Does Research Show About the Effects of Vouchers?

Research findings indicate that vouchers are a highly effective form of housing assistance. A 2002 report by the U.S. General Accounting Office found that vouchers are more cost-effective than federal programs that build affordable housing for low-income households. In addition, research shows that housing vouchers promote positive outcomes for families.

Helping families move out of high-poverty neighborhoods. Vouchers have been shown to help families move from areas with high poverty rates to neighborhoods with lower poverty and higher employment.[8] Researchers have found that using a voucher to move to a low-poverty neighborhood produces a range of positive effects on family well-being, including lower rates of some mental and physical health problems. The effects on mental health — including depression, anxiety, and sleep problems — were particularly striking. By some measures, using a voucher to move to a low-poverty area reduced mental health problems as much as the most effective clinical treatments and medications.[9]

Protecting children from homelessness and housing instability. A 2006 study found that families with children who were issued vouchers experienced significantly lower rates of homelessness compared to a control group, with the strongest effect on families with children under age 6. The same study found that vouchers sharply reduced the number of times families moved from apartment to apartment. Both homelessness and housing instability have been linked to a variety of developmental and health problems in children.[10]

Lifting families above the poverty line. Vouchers substantially reduce the number of families living in poverty (when near-cash income like housing subsidies is taken into account along with cash income), enabling families to spend more on other basic needs. Among the most vulnerable families with children, for example, vouchers have been found to lower the incidence of food insecurity and reduce the number of families that went without dental care because they could not afford it.[11]

Supporting work. Vouchers and other housing assistance play a key role in helping low-income working families make ends meet. Critics have argued that because rents under the voucher program rise as a family’s income increases, vouchers may discourage work. But the most rigorous study to date of families with vouchers refuted this theory, finding no significant negative effect on earnings or employment.[12] Moreover, some studies indicate that vouchers and other housing assistance can promote work, particularly when linked to work incentives and employment services.[13]

Based on such findings, the Bush Administration noted in its fiscal year 2008 budget documents that “based on an assessment of the [voucher] program, this is one of the Department’s and the Federal Government’s most effective programs” and that the program “has been recognized as a cost-effective means for delivering decent, safe, and sanitary housing to low-income families.” The bipartisan, congressionally chartered Millennial Housing Commission strongly endorsed the voucher program in its 2002 report, describing the program as “flexible, cost-effective, and successful in its mission” and calling for a substantial increase in the number of vouchers.

End Notes:

[1] U.S. Department of Housing and Urban Development, Sixth Annual Report to Congress on the Quality Housing and Work Responsibility Act of 1998. Data are for 2004. All households with minor children are counted as “families with children,” even if they also include adults who are elderly or have a disability. Other households where the head or the head’s spouse is 62 or older are counted as elderly, including those with an adult who has a disability. “People with disabilities” includes non-elderly households without children where the head or the head’s spouse has a disability.

[2] CBPP calculation based on HUD data for the first quarter of calendar 2007.

[3] See Douglas Rice and Barbara Sard, “The Effects of the Federal Budget Squeeze on Low-Income Families,” Center on Budget and Policy Priorities, note 21. Available on the internet at https://www.cbpp.org/2-1-07hous2.htm.

[4] Affordable Housing Needs 2005: Report to Congress and Affordable Housing Needs 2003: Report to Congress, both published by the Office of Policy Development and Research, U.S. Department of Housing and Urban Development, available at www.huduser.org.

[5] In years when no incremental vouchers were funded, the share of vouchers that turned over and were reissued to new families has varied from 9 percent to 14 percent. U.S. Department of Housing and Urban Development, Sixth Annual Report to Congress on the Quality Housing and Work Responsibility Act of 1998.

[6] National Low Income Housing Coalitions, “A Look at Waiting Lists: What Can We Learn from the HUD Approved Annual Plans?” NLIHC Research Note #04-03, October 1, 2004.

[7] Barbara Sard and Martha Coven, “Fixing the Housing Voucher Formula: A No-Cost Way to Strengthen the ‘Section 8’ Program,” Center on Budget and Policy Priorities, November 1, 2006, available at https://www.cbpp.org/11-1-06hous.htm.

[8] Gregory Mills et al., “Effects of Housing Vouchers on Welfare Families,” prepared by Abt Associates for the HUD Office of Policy Development and Research, 2006.

[9] Jeffrey R. Kling, Jeffrey B. Liebman, and Lawrence F. Katz, “Experimental Analysis of Neighborhood Effects,” Econometrica, 75-1, January 2007.

[10] Mills et al., 2006

[11] Mills et al., 2006.

[12] Mills et al., 2006. Initial findings from the study that were reported in 2004 indicated that families experienced a small negative effect on employment shortly after they first received their vouchers. When later data became available, however, they showed that over a three-and-a-half-year period, vouchers had no significant impact — either positive or negative — on employment.

[13] Robert C. Ficke and Andrea Piesse. “Evaluation of the Family Self-Sufficiency Program: Retrospective Analysis, 1996-2000,” prepared by Westat for the HUD Office of Policy Development and Research, 2004.

Howard S. Bloom, James A. Riccio, and Nandita Verma, “Promoting Work in Public Housing: The Effectiveness of Jobs Plus,” Manpower Demonstration Research Corporation, March 2005. |