A HAND UP

How State Earned Income Tax Credits Help Working

Families Escape Poverty in 2004

Summary

By

| PDF of

this summary A Hand Up: PDF full report |

| If you cannot access the files through the links, right-click on the underlined text, click "Save Link As," download to your directory, and open the document in Adobe Acrobat Reader. |

Earned Income Tax Credits provide tax reductions and wage supplements for low- and moderate-income working families. The federal tax system has included an EITC since 1975, with major expansions in 1986, 1990, and 1993, and an additional expansion in 2001. In 2002, more than 21 million families and individuals filing federal income tax returns — nearly one out of every six families who file — claim the federal EITC.

The EITC has been widely praised for its success in supporting work and reducing poverty. The federal credit now lifts more children out of poverty than any other government program. Some 4.9 million people, including 2.7 million children, were removed from poverty in 2002 as a result of the federal EITC. The federal EITC also has been proven effective in encouraging work among welfare recipients; studies show it has a large impact in inducing more single mothers to work. Support for the EITC has come from across the political spectrum.

The success of the federal EITC has led a number of states to enact state Earned Income Tax Credits that supplement the federal credit.

-

Eighteen states have created state EITCs based on the

federal credit. In addition,

-

Despite the current challenging fiscal environment, when

most states have been cutting spending, raising taxes, or both, one state

has added an EITC and most states with EITCs have protected or even

expanded them.

- The continuing growth of state EITCs suggests that many state policymakers recognize the continuing importance of an EITC in difficult economic times. At a time of high unemployment and declining wages, state EITCs can help working families stay afloat. And when states are raising taxes in ways that may be burdensome to low-income families, state EITCs can relieve some of that burden.

Why Consider a State EITC?

Several developments explain the popularity of state EITCs, including the continued prevalence of poverty among children, the importance under welfare reform of supporting families’ transition from welfare to work, and interest in tax changes that promote tax fairness.

State EITCs Reduce Poverty Among Children

In 2002, the Census Bureau reported that about one child in six still lived in poverty. Most poor children lived in families with a working parent.

- Some 4.9 million families with children in which the parents were not elderly or disabled had incomes below the federal poverty line.[1] In 66 percent of these families, at least one parent was working.

- About 12.6 million people, including 7.2 million children, lived in working poor families. In 2004 dollars, that means living on less than about $15,100 for a family of three or $19,000 for a family of four.

- High unemployment and declining real wages likely have continued to increase poverty among working families in 2003 and 2004.

Earned Income Tax Credits can lift families out of poverty by supplementing their wages.

- For example, a family of four with two children and a full-time, year-round worker earning about $7 per hour (well above minimum wage) has wages after payroll taxes of about $13,600 per year, several thousand dollars below the poverty line.

- Such a family in 2004 qualifies for a federal EITC of $4,300 and a small federal child tax credit of $395, bringing its income close to the poverty line.

- If the family lived in a state that offered a state EITC set at 20 percent of the federal credit, the family would receive an additional $860, for total cash income of $19,130 — slightly above the poverty line. An EITC set at a larger percent of the federal credit could raise the family’s income further above the poverty line.

State EITCs Complement Welfare Reform

Although large numbers of welfare recipients have entered the workforce, many cannot make ends meet on their earnings alone. State EITCs support families who enter and remain in the workforce.

- Many welfare recipients who take jobs continue to have very low incomes, often below poverty. Studies show that welfare recipients who find jobs typically earn $2,000 to $3,000 per quarter, or $8,000 to $12,000 per year, well below the poverty line for a family of three. The combination of the federal EITC and a state EITC can close the poverty gap for many welfare recipients as they move into the workforce.

- State EITCs also support the work efforts of low- and moderate-income families who have long since left the welfare rolls or who have never received welfare benefits. EITCs help meet the ongoing expenses associated with working, such as transportation, and may allow families to cope with unforeseen costs that otherwise might drive them onto public assistance.

- Research shows that many EITC recipients use their EITC refunds not only to meet day-to-day expenses but also to make the kinds of investments — paying off debt, investing in education, obtaining housing — that enhance economic security and promote economic opportunity.

State EITCs Provide Needed Tax Relief During Times of Fiscal Stress

State EITCs also pay a role in shaping state tax systems. A number of states are responding to weak fiscal conditions by increasing taxes and fees. Enacting a state EITC is a way to reduce, or at least avoid increasing, the already-substantial burden of state and local taxes on the poor.

- In 18 of 42 states with a personal income tax, working poor families with children may pay income taxes. For a two-parent family of four in the states that taxed the poor in 2003, the average income tax threshold — the point at which families began owing tax — was $13,800, some $5,000 below the poverty line for a family of four. The average tax on a family with income at the poverty line was $245.[2]

- In addition, most states rely heavily on sales, excise, and property taxes, with the result that state tax systems are quite regressive. In 2002, the average state and local tax burden on the poorest fifth of married, non-elderly families was 11.4 percent of income. By contrast, the average burden on the wealthiest one percent of such families was 7.3 percent of income.[3]

- When states face difficult fiscal times, they often increase these regressive taxes. State EITCs help reduce tax regressivity and help poor families meet their tax obligations.

Designing a State EITC

Table 1 lists the states that have enacted Earned Income Tax Credits.

-

Illinois, Indiana, Iowa, Kansas, Maine, Maryland,

Massachusetts, New Jersey, New York, Oklahoma, Oregon, Rhode Island,

Vermont, Virginia, Wisconsin, and the District of Columbia

offer EITCs that piggyback on the federal EITC; these 16 states use

federal eligibility rules and express the state credit as a specified

percentage (anywhere from 5 percent to 50 percent) of the federal

credit. By setting the state credit as a flat percentage of the federal

credit, states make the state credit fairly simple for taxpayers to

compute.

- Most of those states — Colorado, the District of Columbia, Illinois, Indiana, Kansas, Maryland, Massachusetts, Minnesota, New Jersey, New York,

|

Table 1 |

||

|

State |

Percentage of Federal Credit |

|

|

Refundable credits: |

||

|

Colorado |

10% (currently suspended; projected to be reinstated in 2006) |

|

|

Dist. of Columbia |

25% |

|

|

Illinois |

5% |

|

|

Indiana |

6% |

|

|

Kansas |

15% |

|

|

Maryland* |

20% |

|

|

Massachusetts |

15% |

|

|

Minnesota |

Varies with earnings; average 33% |

|

|

New Jersey |

20% (if income < $20,000) |

|

|

New York |

30% |

|

|

Oklahoma |

5% |

|

|

Vermont |

32% |

|

|

|

4% — one child |

|

|

Wisconsin |

14% — two children |

|

|

|

43% — three children |

|

|

Non refundable credits |

||

|

Iowa |

6.5% |

|

|

Maine** |

4.92% |

|

|

Oregon |

5% |

|

|

Rhode Island*** |

25% |

|

|

Virginia |

20% effective in 2006 |

|

|

*Maryland also offers a

non-refundable EITC set at 50 percent of the credit. Taxpayers in

effect may claim either the refundable credit or the non-refundable

credit, but not both. |

||

-

Oklahoma, Vermont and

- Five other states — Iowa, Maine, Oregon, Rhode Island, and Virginia — offer “non-refundable” credits that limit the amount of a credit to a family’s income tax liability. A non-refundable EITC can provide substantial tax relief to some families that have income too low to owe state income taxes. A non-refundable credit assists fewer working-poor families with children and is less likely to be an effective work incentive.[4]

- States increasingly prefer the advantages of a refundable credit. Ten of the 13 state credits that have been enacted or expanded since 2000 — the credits in Illinois, Indiana, Kansas, Maryland, Massachusetts, New Jersey, New York, Oklahoma, Vermont, and the District of Columbia — are refundable.

- The federal EITC provides a somewhat larger credit to families with two or more children than to families with just one child, in recognition of the increased cost of living for large families. One state, Wisconsin, goes further: It provides a small state EITC to families with one child, a larger state EITC to families with two children, and a much larger state EITC to families with three or more children.

Financing a State EITC

The cost of a state EITC depends

principally on four factors: the number of families in a given state

that claim the federal credit, the percentage of the federal credit at

which the state credit is set, whether the credit is refundable or

non-refundable, and how many state residents who receive the federal

credit learn about and claim the state credit. Because state EITCs are

well targeted to low- and moderate-income working families, the cost may

be relatively modest. The annual cost of refundable EITCs ranges from

about $14 million in

York

|

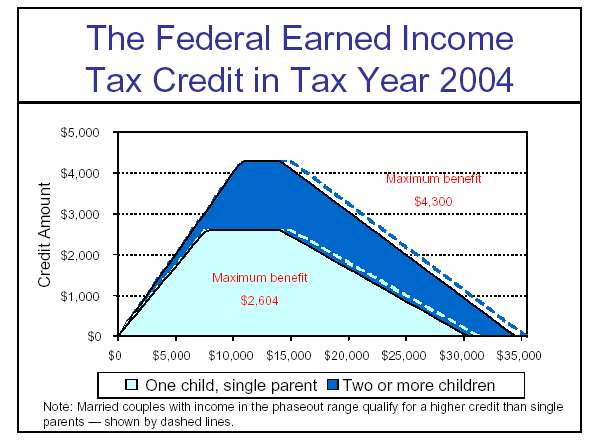

How the EITC Works The federal Earned Income Tax Credit goes only to households with earnings, with the size of the credit initially rising as earnings increase. The credit is capped at $4,300 for a family with two children and $2,604 for a family with one child; the credit then phases out gradually. Families with two children may qualify if their incomes are as high as $35,458. The credit is phased out at a slightly higher income level for married couple families than for other families. Low-income workers without a qualifying child also may receive a federal EITC, but the maximum credit for individuals or couple without children is $390 in 2004, much lower than the credit for families with children. The chart above illustrates the structure of the credit for families with children. Most state EITCs are structured in the same way as the federal credit except that the amount of credit at each income level is lower. The table below shows the amount of federal and state credit for families at various income levels.

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Most state credits to date have been

financed from funds available in a state’s general fund — the same

funding source typically used for other types of tax cuts. When an EITC

is used to offset the effects of a regressive tax increase, such as a

sales tax increase, as it has been in

|

Refundable State EITCs Can Enhance Efforts to Help Families Build Assets a Research indicates that tax refunds, including state EITC refunds, can be used to promote asset building in low-income families. Data from various studies indicate that many low-income individuals value saving and assets. For example, research suggests that low-income individuals can save and accumulate assets in Individual Development Accounts (IDAs). b IDAs are special savings accounts designed to help low-income individuals build assets to reach certain goals such as buying a home, pursuing post-secondary education, or starting a business. In addition, there is evidence that some low-income families save part of their tax refunds; one study found, for example, that 33 percent of the 650 EITC recipients examined planned to save a portion of their tax refunds. c This suggests that tax refunds might be effectively linked to a variety of asset-building initiatives. a For more information see “Promoting Asset Building through the Earned Income Tax Credit,” State IDA Policy Briefs, Vol. 1, No. 1, Center for Social Development and Corporation for Enterprise Development. b Schreiner, M., Clancy, M. & Sherraden M. Saving performance in the American Dream Demonstration. St. Louis, MO: Washington University in St. Louis, Center for Social Development, 2002. c Smeeding, T.M., Phillips, K. R., & O’Conner, M. “The Earned Income Tax Credit Experience: Expectation, knowledge, use, and economic and social mobility.” National Tax Journal, 53 (4, Part 2), 1187-1209 |

[1] These figures were tabulated from the U.S. Census Bureau’s Current Population Survey, March 2003. An additional 600,000 poor families had parents who were ill, elderly or disabled, and thus were not able to work.

[2] Center on Budget and Polity Priorities, State Income Tax Burdens on Low-Income Families in 2003. April 2004. This report is updated annually.

[3]

Institute on Taxation and Economic Policy, Who Pays?: A

Distributed Analysis of the Tax Systems in

[4]