HOW WOULD THE PRESIDENT’S NEW SOCIAL SECURITY PROPOSALS

AFFECT MIDDLE-CLASS WORKERS AND SOCIAL SECURITY SOLVENCY?

by Jason Furman

| PDF of full report |

| If you cannot access the files through the links, right-click on the underlined text, click "Save Link As," download to your directory, and open the document in Adobe Acrobat Reader. |

Summary

In a press conference on April 28, President Bush endorsed a proposal that would result in substantial cuts in benefits for middle-income families and deeper cuts for higher-income families. While the proposal was described as reducing benefits for the most affluent Americans, it would result in large benefit reductions for middle-class workers, as well.

- All workers with income above $20,000 today would be subject to benefit reductions. Seven of every ten workers would be affected. (Robert Pozen, the investment executive who designed this proposal, generally describes the cut-off as $25,000, but that is because he is using the expected cut-off in 2012, and expressing in 2012 dollars.)

- The benefit reduction for middle-class workers would be large. The size of the benefit reductions would escalate sharply in size as income rose above $20,000, until income reached $90,000. A worker making $35,000 today would be subject to benefit reductions more than half as large as those imposed on people at the highest income levels. A worker making $60,000 today would be subject to benefit reductions that are nearly as large (as a percentage of his or her promised benefits) as the reductions that would be imposed on someone making several million dollars a year. (See Table 1.) For a $60,000-a-year worker who retires in 2045, the benefit cut would equal 25 percent, or about $6,500 a year.

- Social Security survivor benefits would be cut by the same magnitude. How disability benefits would be affected is unclear. (See below.)

- For many workers, cuts would be deeper than if no action were taken and Social Security became insolvent. The Social Security Trustees project the Social Security Trust Fund will be depleted in 2041. (The Congressional Budget Office projects this will occur in 2052.) The President has repeatedly characterized 2041 as the year when the system becomes “bankrupt” (an inaccurate characterization because the system would still pay 74 percent of scheduled benefits at that time). Yet for workers who now make about $55,000 or more, Social Security benefits would be cut more deeply under the benefit-reduction proposal the President now has endorsed than if nothing were done to restore Social Security solvency.

- The benefit reductions for average earners would be the largest in Social Security’s history. The 1983 Social Security reform, for example, lowered benefits for average workers by 17 percent, with the reduction phased in over 46 years. The President’s plan would lower benefits for average workers by 28 percent over a period of 70 years — and by considerably more than that for middle-class workers with incomes somewhat above the average, such as those who make $60,000 today.

|

Reduction in Benefits Under |

||

|

|

Dollar Reduction |

Percentage Reduction |

|

Earnings of $36,600 |

|

|

|

Worker retiring in 2045 |

$-3,253 |

-16% |

|

Worker retiring in 2075 |

-7,629 |

-28% |

|

Earnings of $58,560 |

|

|

|

Worker retiring in 2045 |

-6,444 |

-25% |

|

Worker retiring in 2075 |

-15,154 |

-42% |

|

Earnings of $90,000 or more |

|

|

|

Worker retiring in 2045 |

-9,324 |

-29% |

|

Worker retiring in 2075 |

-21,808 |

-49% |

|

Source: Authors calculations based on Social Security Administration, Office of the Chief Actuary, “Estimated Financial Effects of a Comprehensive Social Security Reform Proposal Including Progressive Price Indexing -- INFORMATION,” February 10, 2005 and Social Security Trustees, 2004 Annual Report. All percentage reductions in benefits for 2025-2075 are taken directly from the actuaries’ memo |

||

Why the Benefit Reductions Are So Large

That the proposal entails such large benefit reductions for workers who are not affluent is the result of the President’s apparent insistence on closing most or all of the solvency gap through benefit cuts, rather than — as was done in 1983 — through a balanced mix of benefit changes and new revenues. Under a balanced approach, benefit cuts of this severity could be averted.

Moreover, the plan is considerably less progressive than the President has presented it as being. The progressive price indexing proposal that the President has embraced applies the same size benefit reduction to people who make $90,000 as to people who make $9 million, and workers making $60,000 would be subject to a reduction nearly as substantial. A more balanced and progressive approach that included new revenues from those who could afford to pay them could restore sustainable solvency with significantly smaller benefit cuts for middle-class retirees and no net benefit cuts for people with disabilities.

Effects on Disability Benefits

The President’s

proposed change in the

|

Defined Social

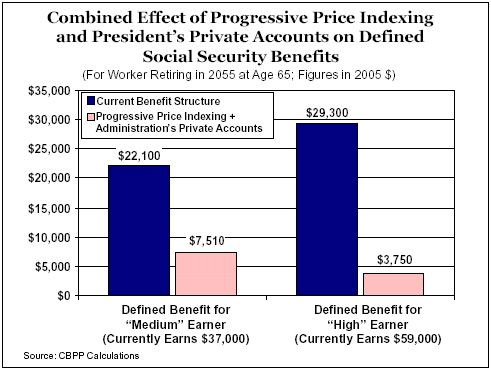

Security Benefits Would be Lowered Further The President’s proposal, as it now stands, combines Robert Pozen’s “progressive price indexing” proposal with private accounts. The President has proposed that workers be allowed to divert payroll taxes equal to four percent of their wages from Social Security into private accounts. The cost of these accounts would be offset by reducing substantially the Social Security benefits of those who elect the accounts. As a result, under the President’s plan, defined Social Security benefits (for people electing the accounts) would be lowered twice — once due to the indexing changes, and a second time to pay for the accounts. The resulting reduction in the Social Security benefits of those who elect the private accounts would be extremely large. Under the combination of the Pozen “progressive price indexing” proposal that the President has embraced and the President’s private accounts, the defined Social Security benefit would be reduced by 66 percent — from $22,100 a year to $7,510, in 2005 dollars — for a medium earner who retires in 2055. For a worker who earns 60 percent above the average wage, the reduction in Social Security benefits would be 87 percent — from $29,300 a year to $3,750 (in 2005 dollars). In addition to this greatly reduced defined benefit, the worker also would get a private account that was subject to market risk. Moreover, these figures reflect Social Security benefits before Medicare premiums are subtracted. (Medicare premiums are collected by being subtracted from Social Security checks.) Since Medicare premiums grow at the rate of health care costs, which is faster than either prices or wages, they will consume a steadily increasing share of Social Security benefits over time. For many middle-income workers, Medicare premiums would consume most or all of the very small monthly Social Security benefit that would remain under the combination of progressive price indexing and the President’s private accounts. Social Security checks for millions of ordinary American workers thus would be close to or at zero.

|

The

White House issued a fact sheet April 28 stating that its proposals, too,

would close 70 percent of

It should be

noted that if the President’s plan does protect disability benefits,

many disabled beneficiaries apparently would still be subject to

benefit cuts. Under

How the Pozen Proposal Works

Mr. Pozen has

proposed changing the formula used to calculate

More

specifically, the Pozen plan would reduce certain factors used to calculate

benefits for retirees, people with disabilities, and survivors (e.g., children

of workers who die prior to retirement).[3]

As a result, those receiving survivors and disability benefits would be

affected.

According to Pozen, his plan would “close the long-term deficit of

As noted, about one-sixth of the improvement in solvency in the Pozen proposal comes from reductions in disability benefits.[7] A similar amount of the solvency improvement from the Pozen plan is the result of reductions in benefits for survivors, including children who get benefits as a result of the death of a parent prior to retirement. The remainder comes from reductions in retirement benefits.

To Protect People With Disabilities, the President Would Need to Increase Pozen’s Benefit Cuts for Retirees and Survivors by About One-fifth

The White House

fact sheet states the President’s “reform would solve approximately 70 percent

of the funding problems facing

Protecting

people with disabilities would result in about one-sixth less in solvency

improvement than the original Pozen proposal. In addition, the President

proposed a new minimum benefit for poor seniors, which would add a further,

albeit modest, cost. If the proposal to shield disability benefits and the

proposed minimum benefit are coupled with the Pozen plan’s benefit reductions

for retirees and survivors, the President’s proposal would eliminate 59

percent of

For the White House statement that its plan would solve 70 percent of the deficit “by adopting a sliding-scale benefit formula, similar to the Pozen approach” to be correct if disablility benefits are protected, the White House would have to make the Pozen sliding scale more severe so that benefit cuts for retirees and survivors would be roughly one-fifth larger than those that would occur under the Pozen plan.

Larger benefit

cuts for retirees and survivors may not be part of the President’s

plan. If so, the plan will not close anywhere near 70 percent of the 75-year

The Size of the Benefit Reductions Under the Pozen Proposal

Under

the current benefit structure, initial

The Pozen proposal would use price indexing to determine the benefits for “maximum earners,” people who currently make $90,000 or more a year. Lower-earners — the bottom 30 percent of earners, or those who make less than about $20,000 currently — would continue to have their benefits calculated under the current formula. Anyone whose annual earnings over his or her career averaged between $20,000 and $90,000 would get a benefit somewhere between the currently promised benefit and the benefit that would be provided under full price indexing.

Estimates of Mr. Pozen’s plan by the

For a worker whose wages are 60 percent above those of the average worker, or about $59,000 in 2005, the benefit reductions under the Pozen proposal would grow from 25 percent — or $6,444 a year — for someone retiring in 2045, to 42 percent — or $15,154 a year — for someone retiring in 2075. For a maximum earner — someone who makes $90,000 or more in 2005 — the benefit reductions would grow from 29 percent, or $9,324 annually, for an individual retiring in 2045 to 49 percent, or $21,808, for someone retiring in 2075. (See Table 2.)

As these

figures indicate, the benefit cuts for someone at $59,000 a year are nearly as

large as those for someone who makes $90,000, or $900,000, or even $9 million

a year. (Note: benefits under the current benefit structure are the most

appropriate frame of reference for a variety of reasons, as discussed in the

Appendix. Most fundamentally, these are the benefit levels that are used to

calculate the

President’s Plan is Not Balanced

The

President’s plan includes benefit reductions of this magnitude because it

places most of the burden of closing the

|

Social Security Benefits Under Progressive Indexing For Workers Retiring at Age 65 In Various Years (inflation-adjusted 2005 dollars) |

||||||

|

|

Current-law Formula |

Proposal |

Change |

|||

|

|

Benefit |

Replacement Rate |

Benefit |

Replacement Rate |

Dollar Reduction |

Percentage Reduction |

|

Scaled Low Earner (45 percent of the average wage, or $16,470 in 2005) |

||||||

|

2025 |

$9,718 |

49% |

$9,718 |

49% |

$0 |

0% |

|

2045 |

12,041 |

49% |

12,041 |

49% |

0 |

0% |

|

2075 |

16,599 |

49% |

16,599 |

49% |

0 |

0% |

|

2100 |

21,820 |

49% |

21,820 |

49% |

0 |

0% |

|

|

|

|

|

|

|

|

|

Scaled Medium Earner (average wage, or $36,600 in 2005) |

||||||

|

2025 |

16,009 |

36% |

14,984 |

34% |

-1,025 |

-6% |

|

2045 |

19,837 |

36% |

16,584 |

30% |

-3,253 |

-16% |

|

2075 |

27,344 |

36% |

19,715 |

26% |

-7,629 |

-28% |

|

2100 |

35,945 |

36% |

22,428 |

23% |

-13,518 |

-38% |

|

|

|

|

|

|

|

|

|

Scaled High Earner (160 percent of the average wage, or $58,560 in 2005) |

||||||

|

2025 |

21,228 |

30% |

19,190 |

27% |

-2,038 |

-10% |

|

2045 |

26,302 |

30% |

19,858 |

23% |

-6,444 |

-25% |

|

2075 |

36,254 |

30% |

21,100 |

18% |

-15,154 |

-42% |

|

2100 |

47,658 |

30% |

22,428 |

14% |

-25,230 |

-53% |

|

|

|

|

|

|

|

|

|

Steady Maximum Earner (taxable maximum, or $90,000 in 2005) |

||||||

|

2025 |

25,929 |

24% |

22,999 |

21% |

-2,930 |

-11% |

|

2045 |

32,153 |

24% |

22,829 |

17% |

-9,324 |

-29% |

|

2075 |

44,236 |

24% |

22,428 |

12% |

-21,808 |

-49% |

|

2100 |

58,150 |

24% |

22,428 |

9% |

-35,723 |

-61% |

Indeed, it may be argued that the President’s plan is not progressive enough. As noted, his plan would apply the same magnitude of benefit reductions to a worker whose annual earnings average $90,000 as to one whose annual earnings average $9 million. Someone making $60,000 annually would get about 85 percent as large a percentage benefit reduction as the individual who makes $9 million.

Other

approaches would restore solvency with more balance between benefits and

taxes, and also would take a more progressive approach to restoring

solvency that ensures that people with very high incomes contribute

significantly more than hard-pressed middle-class families. For example, the

solvency plan designed by economists

Similarly, a plan proposed by former

APPENDIX: SHOULD BENEFIT CUTS BE COMPARED TO SCHEDULED BENEFITS?

This analysis

compares

The debate over

- Citing a large Social Security financial shortfall is inconsistent with using “payable benefits” as the standard. The President and other observers frequently say that Social Security faces a $4 trillion shortfall over the next 75 years (or in the President’s more controversial statement, an $11 trillion shortfall over an infinite horizon). These estimates are based on benefits under the current benefit structure. The shortfall under the “payable benefits” baseline is zero. It makes little sense to use one benchmark for assessing Social Security’s financing shortfall and another benchmark for assessing the solutions to the shortfall.

- Using payable benefits contradicts common usage. It is commonly said that restoring Social Security solvency will require benefit reductions, tax increases, or a combination of both. But under a “payable benefits” framework, this statement is incorrect. If only the “payable benefits” are supposed to be provided, there is no financing gap and no benefit cuts or revenue increases are necessary.

- Replacement rates are the appropriate way to compare retirement benefits over long periods of time. Social Security benefits are designed to replace a certain fraction of pre-retirement income. Under the current-law formula, they eventually replace 36 percent of income for the average retiree. Changes that lower this ratio constitute a reduction in benefits: they cause sharper declines in workers’ standard-of-living when workers retire. Using “scheduled benefits” as the standard of comparison reflects this basic aspect of Social Security; using “payable benefits” as the standard does not.

- Benefit changes should be measured relative to the benefits that people expect. People expect benefits calculated under the current Social Security benefit structure. A reduction from that level should be described as what it is, a reduction in benefits relative to the current benefit structure.

- Payable benefits are only one particular framework. The “payable benefits” framework assumes that the entire adjustment to close Social Security’s shortfall is done on the benefits side. A framework could just as well assume that payroll taxes would rise enough to eliminate the deficit. Under such a framework, for example, both the Pozen and Diamond-Orszag plans would be viewed as cutting payroll taxes relative to the levels needed for solvency. In short, adopting the “payable benefits” framework as the basic standard of comparison is arbitrary, as would be the adoption of a framework that simply assumed payroll taxes would be raised enough to eliminate the shortfall.

- Any plan that solves less than 100 percent of the financing problem will generally be able to provide benefits that exceed payable benefits. The White House benefit reduction plan would only solve 59 percent to 70 percent of the 75-year problem in Social Security. In Mr. Pozen’s formulation, the remaining gap is closed by transferring $2 trillion to Social Security from the rest of the budget, even though the rest of the budget will be in deficit for as far as the eye can see and has no surplus funds to transfer. Any plan that does not fully restore solvency can ensure that benefits are higher than payable benefits. In such circumstances, using payable benefits as the principal standard of comparison can foster misleading impressions.

End Notes:

[1]

[2] The Center previously released an estimate that the President’s plan closed 59 percent of the solvency gap. That was based on the 2004 Trustees Report, the report used to score the Pozen plan. This estimate is updated to reflect the assumptions in the 2005 Trustees Report.

[*]The White House appears to be defending its 70 percent claim by saying that its proposal would eliminate 70 percent of the projected deficit in the 75th year of the proposal. This is not the longstanding, widely accepted way of measuring the share of the long-term solvency gap that a Social Security proposal closes. The standard approach is to measure the percentage of the gap that a proposal would close over the next 75 years.

[3]

The factors in question, known as the “PIA factors,” are set at 90

percent, 32 percent, and 15 percent and are applied to a worker’s average

wages over his or her career when the worker’s

[4]

[5]

“Testimony on Progressive Price Indexing,” Robert Pozen,

[6] Specifically, Table 2d of the actuaries memo shows that progressive price indexing would save $2.9 trillion in net present value over the next 75 years, or 1.36 percent of taxable payroll.

[7]

Economists

[8]

See Robert Greenstein, “So-called

“Price Indexing” Proposal Would Result in Deep Reductions Over Time In

Social Security Benefits,”

[9]