JOINT TAX COMMITTEE ESTIMATE SHOWS TAX

CUTS IN NEW STIMULUS PLAN

WOULD HAVE LARGE COSTS AFTER RECESSION ENDS

Proposal Would Widen Budget Debts in

Coming Years

by Robert Greenstein,

Richard Kogan, and Andrew Lee

| PDF

of the report If you cannot access the files through the links, right-click on the underlined text, click "Save Link As," download to your directory, and open the document in Adobe Acrobat Reader. |

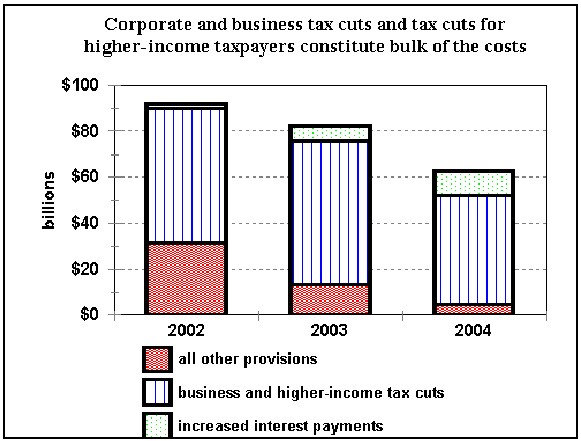

On December 19, the Joint Congressional Committee on Taxation, Congress' official scorekeeper on tax legislation, issued an estimate of the cost of the plan which Rep. Bill Thomas and House leaders brought to the House floor yesterday and the House subsequently passed. The Joint Tax estimate confirms that this package is largely a multi-year tax-cut package, rather than a measure primarily aimed at stimulating the economy now.

- The plan would cost approximately $75 billion in fiscal year 2003 and $50 billion in fiscal year 2004, years when the economy is expected to be in recovery and further stimulus is not expected to be needed. Some 91 percent of the cost in 2003 and 99 percent of the cost in 2004 cost would result from tax cuts.

- Fiscal years 2003 and 2004 are years when the nation already faces deficits in the unified budget. The Administration reportedly is planning to propose cuts in a number of domestic programs in its forthcoming fiscal year 2003 budget on the basis that cuts are needed to help address these troublesome deficits.

- The plan consists overwhelmingly of tax cuts. The Joint Tax Committee estimate indicates that approximately 92 percent of the plan's costs over the next five years and 95 percent of the cost over ten years consists of tax cuts. If the tax rebate and the refundable component of the health tax credit are counted as spending rather than as a tax increase, then 83 percent of the cost over five years and 84 percent of the ten-year cost consists of tax cuts.

- The plan is heavily oriented toward businesses and higher-income individuals. Tax cuts for businesses and those in the top quarter of the income spectrum account for 77 percent of all the plan's costs over the next five years.

- The tax cuts are not well designed as economic stimulus. Only 40 percent of the tax cuts the plan would provide over the next five years would come in fiscal year 2002. Tax cuts in years after 2002 would not stimulate the economy during the downturn. Furthermore, many of the tax cuts that would be provided in 2002 would not be very stimulative themselves, because these tax cuts would go to higher-income individuals — who tend to save rather than spend much of the additional income they receive — and would go to corporations regardless of whether the corporations make new investments now. As a result, only a quite small fraction of the generous tax cuts in this legislation would have any significant effect in helping the economy recover from the downturn or protecting workers from further lay-offs.

- Some of the tax provisions in the package provide nearly all of their tax cuts after 2002. For example, only four percent of the five-year tax cut for financial corporations that have foreign operations would come in 2002; some 96 percent of this tax cut would occur in subsequent years.

| Provision | Five-year cost | Share of the five-year cost occurring in 2002 | Share of the five-year cost occurring in 2003-2006 |

| Tax cut for financial corporations with foreign operations | $6.5 | 4% | 96% |

| Depreciate leasehold improvements over 15 rather than 39 years | $1.9 | 4% | 96% |

| All other extensions of expiring tax provisions | $3.7 | 11% | 89% |

| Corporate and individual AMT reductions | $10.0 | 13% | 87% |

| Accelerate rate reductions in the 27.5% tax bracket and increase the exemption from the individual AMT so the rate reductions do not subject more filers to the AMT | $60.0 | 23% | 77% |

- The total package would cost $214 billion over five years, not counting the additional interest payments on the debt that would have to be made as a result of the package. When the additional interest costs are included, the total cost exceeds $260 billion over five years.

Over ten years, the cost with interest is more than $270 billion, but that number may be deceptively low; it assumes that every one of the multi-year tax cuts in the bill ends on schedule, with none of those tax cuts being extended. That must be regarded as an unlikely scenario.

- The multi-year nature of these tax cuts makes sense only if one of the goals of the legislation is to heighten the chances that these corporate tax cuts will be extended when they are scheduled to expire — and thus will become ongoing fixtures of the tax code. Such a course would add several hundred billion dollars in additional costs over the coming decade.

For example, the package's principal depreciation provision — which would allow businesses to take immediate deductions for 30 percent of the cost of equipment and certain other items they purchase — would be in effect for three years rather than one. As analyses from the Brookings Institution have shown, making this provision effective for three years lessens its stimulative effect, because doing so enables firms to wait a year or more to see what the economy looks like before making purchases; firms would be able to defer making purchases and still secure the tax break. The likely reason for making this provision effective for three years rather than one appears to be that doing so would make it more likely this provision would come to be seen as a normal feature of the tax code and thus would make extension of the provision at the end of the three-year period more probable. Indeed, this tax break is designed so it would expire on September 11, 2004 — shortly before the elections — making it even more likely it would be extended at that time. If this tax break is extended and remains in effect throughout the decade, its cost — according to the Joint Tax Committee — will climb by more than $200 billion over ten years, on top of the costs shown for this provision in the new Joint Tax Committee estimates.